|

|

||||||

| Back to Tax School Homepage | ||||||

|

Tax Topic 6 - Deductions for Taxes

In this topic we will cover the the payment of taxes you can deduct. Usually, you are able to deduct income taxes, general sales taxes, real estate taxes, personal property taxes and foreign taxes paid. You will also become aware of which taxes you can deduct and which taxes you cannot.Student Instructions:Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

Use IRS Publication 514, IRS Publication 17 page 150-155, and Schedule A Instructions on page A-2 for "Taxes You Paid" (also page A-12) to complete tax topic 6. Complete a Schedule A. Then, fill out Form 1040. Use the following expenses:

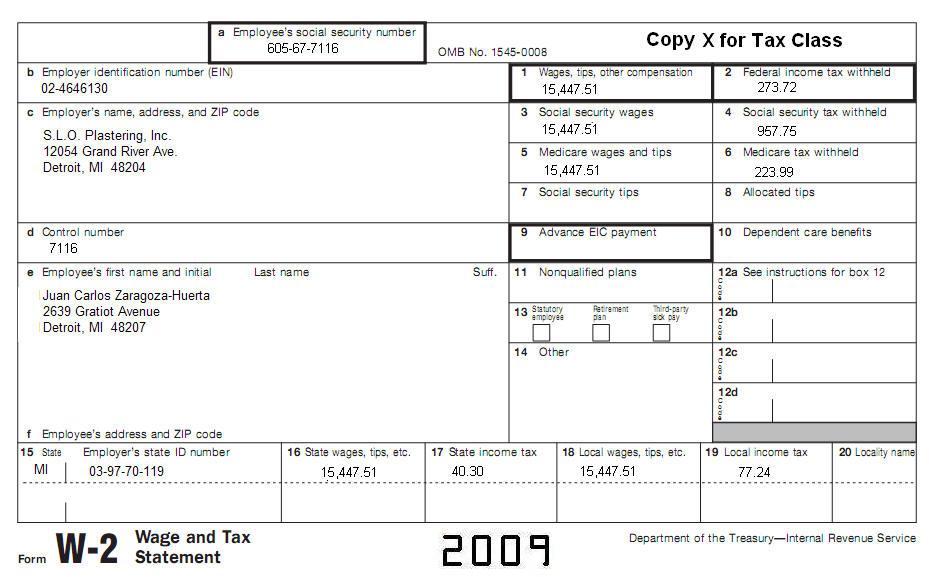

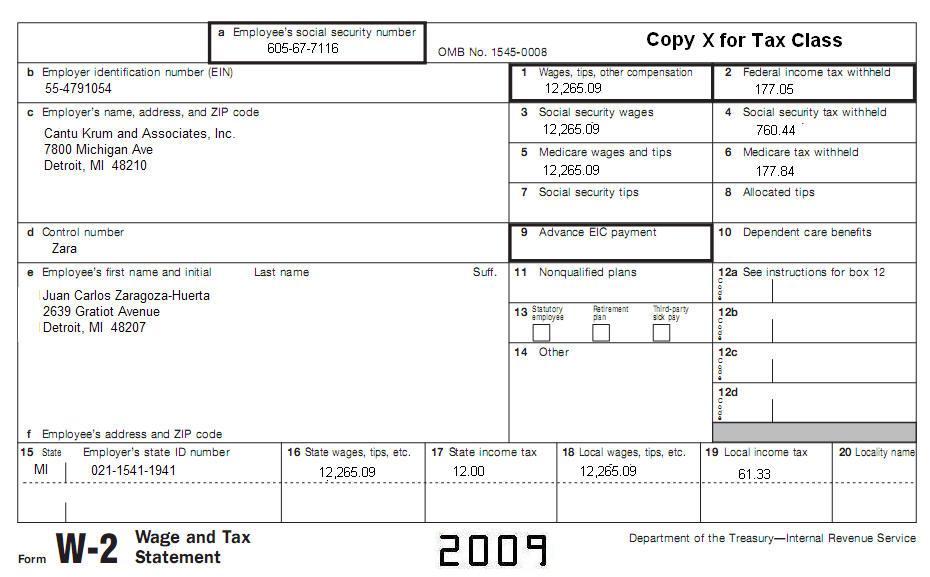

Juan Carlos is not married and has no children or other dependents. All information is current in the following W-2s, including income and address information.

|

||||||

| Back to Tax School Homepage |