|

|

| Back to Tax School Homepage |

|

Tax Topic 29 - Tax Withholding and Estimated Tax

Our federal income tax system is a pay-as-you-go tax. You must pay the tax as you receive the income during the year. In this tax topic you will learn how taxpayers get income withheld from their pay and other income such as pensions, bonuses, commissions, and gambling winnings. However, if no one withholds from your sources of income, you might have to pay estimated taxes such as when the taxpayer is business for himself or herself. A taxpayer may also have to pay estimated taxes on income such as dividends, interest, capital gains, rents, and royalties. In addition, you will learn how to take credit for the withholding on the tax return and calculate the penalties for not paying enough. Student Instructions:Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online Most forms are in Adobe Acrobat PDF format.

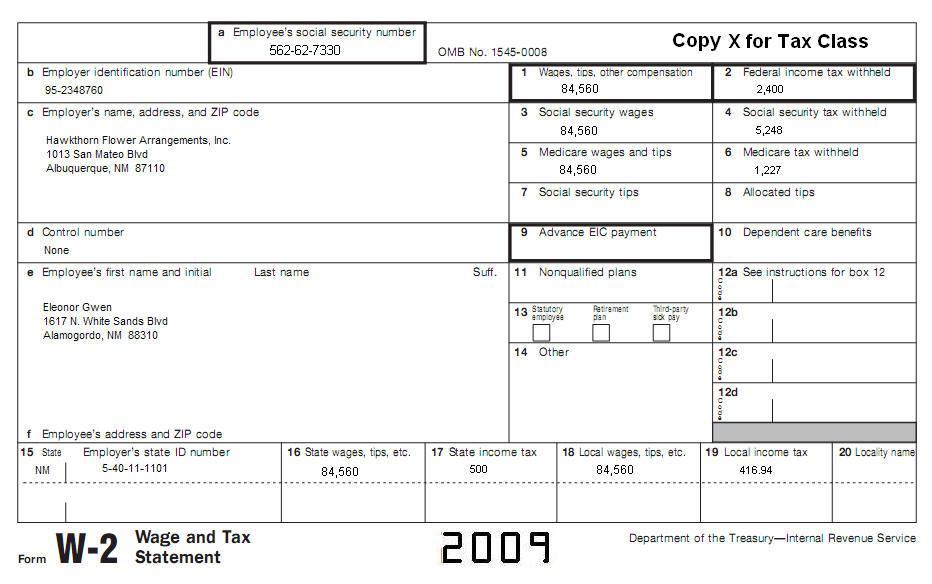

Material needed to complete this assignment:Please use IRS Publication 505 and IRS Publication 515 to complete this topic. You may also need instructions for Form 1040. Prepare Form 1040 and Form 2210 (if needed) for Eleonor Gwen. She is single and has no dependents. In tax year 2008 Eleonor did not have a tax liability. However, for 2009, Eleonor worries that she may owe a penalty for underpayment of her tax.

|

| Back to Tax School Homepage |