|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Back to Tax School Homepage | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Tax Topic 21 - Deducting Business Expenses

In this tax topic you will learn how deduct common business expenses and what is and is not deductible. In this tax lesson you'll also become aware of the specific expenses that are deductible. Business expenses are the costs of carrying on a business and they are normally deductible as long as the business is operated to make a profit. Here, you will learn what you can deduct, and how much to deduct when there are limits and when you can deduct the business expenses. In addition, you will encounter information on not-for-profit activities and the limitations imposed on them. Student Instructions:Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online Most forms are in Adobe Acrobat PDF format.

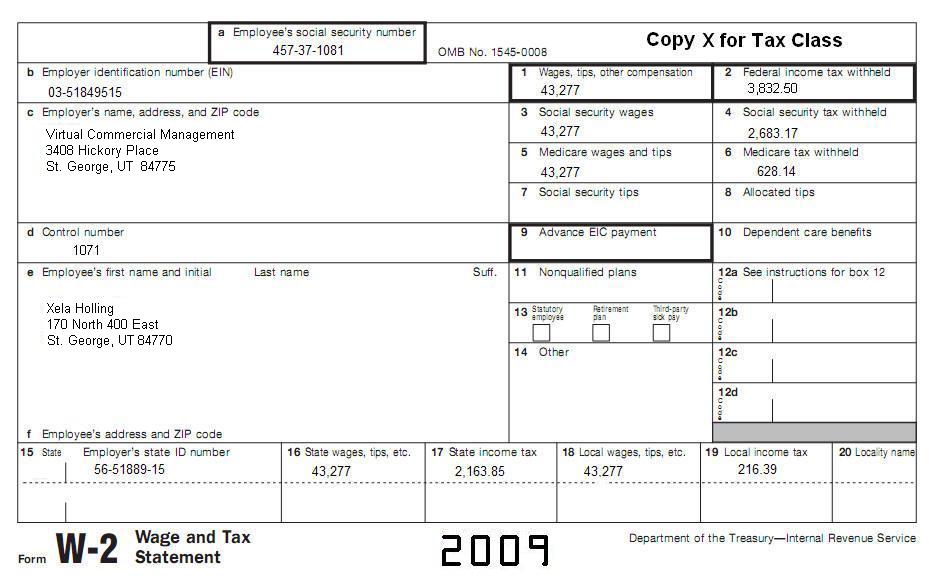

Material needed to complete the sections in this assignment:Please use IRS Publication 535 to complete this topic. Use the appropriate forms to complete a tax return for Xela Holling: Form 1040 (You may also need Form 1040 Instructions), Schedule A, Schedule C, Schedule SE, for this topic. Xela Holling enjoys making masks. She learned to make masks two years ago in November at the "Dia De Los Muertos" celebration while visiting her parent's home town Chichicastenango, in Guatemala. She fell in love with the different varieties of masks that she saw people wearing for the celebration. As a result she started making her own masks once she was back in the U.S. She would dedicate her weekends for her passion. Some weekends she is not able to dedicate it to her mask making work because she has to work overtime at her regular job. She does make money from the masks as word got around that she creates such beautiful work. Although her art is suitable for wear, most of her customers buy it for wall decoration and display. Once in a while she rents a small space at the local flea-market to display her art and sometimes even at the local museum and auctions. As a result of this, she makes numerous sales. She also displays her work online. She never imagined ever making money from something that she does not consider work. In 2009, she had the following from her mask making activities:

*Xela was forced to acquire a business license as she had received a penalty in 2009 for not having one. In addition, Xela pays a mortgage and had the following in 2009:

Xela was not married and did not have any dependents in 2009. Get all basic information from the following W2, including income information.

What is the amount Ms. Smith may deduct as real estate taxes on her commercial real estate for 2009?

A. $2,955. 10. Sandy and Buffy formed the S&B Partnership in November of 2008. They began business operations in December 2009. During 2009 they incurred the following costs:

What is the maximum dollar amount that S&B Partnership can elect to amortize as organizational costs?

A. $3,750. 11. Which of the following fringe benefits for meals is subject to the 50% deduction limit?

A. Meals furnished to your employees at the work site when you operate

a restaurant. 12. Which of the following would not qualify for a percentage depletion deduction?

A. Gas well. 13. Michael James purchased a travel agency on July 1, 2009, and immediately took over the business. The purchase contract included the following items as part of the purchase price:

What is the proper amount of Michael's Internal Revenue Code 197 amortization expense for 2009 assuming Michael is a calendar year taxpayer?

A. $90,000. 14. In 2008, Rex, a sole proprietor of Bay View Wrecking, had gross income of $200,000, a business bad debt deduction of $6,000, and other expenses of $156,000. Bay View Wrecking employed the accrual method of accounting and used the specific charge-off method for bad debts. In 2009, Bay View Wrecking recovered $4,500 of the $6,000 previously deducted in 2008. What is the correct way for Rex to report this recovery?

A. Report $4,500 as "Other Income" on Schedule C in 2009. 15. The FX Partnership manufactures garden hoses for sale. In the month of January, its sales were $80,000. During that month, the partnership had:

What is the cost of goods sold for the FX Partnership for the month of January?

A. $58,000. 16. Matt and Jason, Partners in the M & J Partnership began business on June 15, 2009. The business incurred the following expenses prior to June 15th:

What is the cost of improvements?

A. $108,500. 17. Between November 1 and December 1, 2009, you paid a total of $52,000 in start-up costs to create a new business. The business opened its doors on December 15, 2009. Which of the following is a permissible election for treatment of the $52,000 in start-up costs you paid?

A. Amortize $52,000 over a 15-year period. 18. Richard, a self-employed attorney, began a fishing guide business in 2003. He reports income and expenses from this fishing guide activity on a Form 1040 Schedule C separate from his reported earnings as an attorney. The fishing guide business reported net losses each year while Richard's attorney business showed significant net earnings in each of the years from 2003 to 2008. In 2009 Richard's business as an attorney showed a net profit of $50,000. Richard's fishing guide business had the following income and expenses in 2009:

Richard has itemized deductions that he will report on Schedule A of his 2009 Form 1040. How much depreciation deduction can Richard report from his fishing guide business activity in 2009?

A. $(3,000). 19. In 2009, John and George formed a partnership that began business on July 2009. They spent $4,000 in legal fees for negotiating and preparing the partnership agreement, $2,000 for accounting services setting up the partnership books, and $1,000 in commissions associated with acquiring assets for the partnership. They made a proper election to amortize organization expenses over a 180 month period. Assuming these are their only expenses in starting their partnership, what is the proper amortization expense for 2009?

A. $1,000. 20. As of December 31, 2008, Doyle, Inc. had incurred $6,000 in potential market feasibility costs, $3,600 in legal fees for setting up the corporation, $2,400 in advertising costs for the opening of the business, and $18,000 for the purchase of equipment. Doyle, Inc. began business operations on January 1, 2009. If Doyle, Inc. chooses to amortize its organizational and start-up expenses over the minimum 180-month period, how much can Doyle, Inc. deduct as an amortization expense in 2009?

A. $800.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Back to Tax School Homepage |