![]()

![]()

Tax School Homepage

Student Instructions:

Please follow the following 3 steps:

1. Read the reading Material to answer the questions on this page and also to complete the short quiz. Reading Material click here.

2. Submit Assignment Online Click Here. (Have your questions on this page filled out and ready to answer the questions online one by one).

3. Complete a short quiz on the reading material: Short Quiz online click here. You have 25 minutes to complete 15 questions for this quiz. You must study the reading material. You won't have time to look up questions in the reading material. If you don't pass, you can retry - Every time you try the questions will be different.

So just to recap: for every section or topic you will submit an assignment (step 2) and a short quiz (step 3). Once these two items are submitted, a certificate will be issued to you.

Important: If you fail a topic you can try again until you pass. However, you cannot try again until 24 hours later. This will give you enough time to study and review the reading material.

Use IRS Publication 970 to answer the following questions. You may also need Form 1040 Instructions.

Complete Form 1040, Form 8863 for this topic.

Maria's family goes to school.

| Maria's daughter, Leticia Gonzalez, paid $2,000 for tuition fees for herself to attend a qualifying community college full time. Leticia had expenses used to claim the Hope credit in the previous two years. | |

| Her son, Raul Gonzalez, also paid $1,800 tuition fees to attend the same community college full time. However, Raul only attended school for about a month, and he was not eligible for a refund of fees paid. | |

| Her children are her dependents and she claims them on her return. | |

| Leticia's SSN is 555-10-7500 and her date of birth January 20, 1990. | |

| Raul's SSN is 555-10-7501 and his date of birth February 20, 1991. | |

| This is the first year Raul attends college. Both Leticia and Raul are enrolled to pursue their degrees. |

Maria is a not married. She provides a home for her son and daughter. She is the only one that can claim her children and provided for her family by herself. No one can claim her or her children as dependents.

She paid rent all year for a of $9,600.00.

Maria received a tax-free scholarship from Women for Education Inc. The amount she received was $3,000 towards her studies to get a nursing degree at the same community college her kids attend. All the money was for enrollment and attendance as specified by the school.

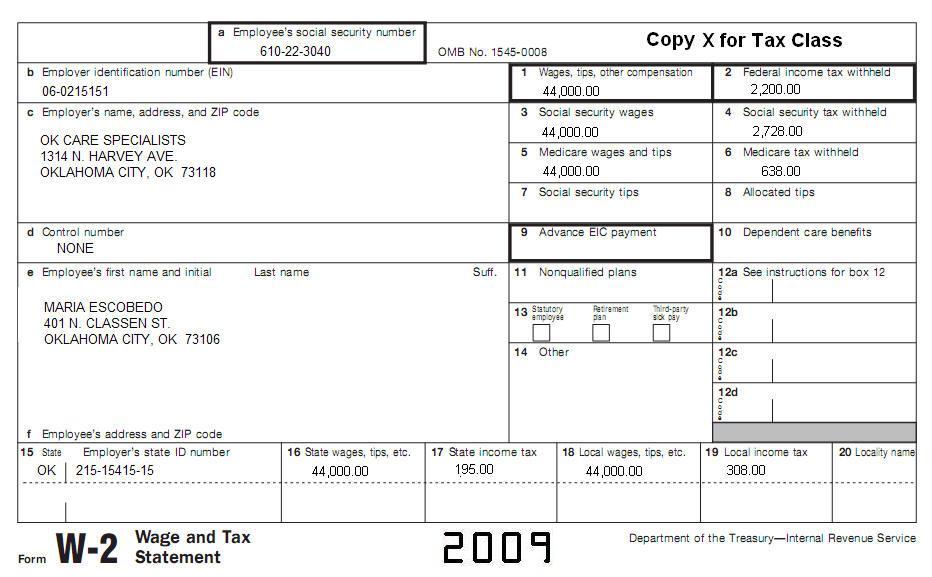

Get all basic information from the following W2, including income information.

![]()