Tax Topic 8 - Tax

Deduction for Job Expenses and other items

In this topic you will cover which

expenses are subject to the 2% limit and which expenses are not. You

will also learn which expenses you cannot deduct and how to report the

expenses that are deductible. For example, some of the expenses that are

deductible are unreimbursed employee expenses that are incurred during

the year and that are ordinary and necessary.

Student Instructions:

Print this page, work on the questions and then submit test by

mailing the answer sheet or by completing quiz online.

Most forms are in Adobe Acrobat PDF format.

You

will need Adobe Reader to view and print these forms. If you do

not already have Adobe Reader installed on your computer, you may

download the software for free.

Use IRS Publication 529 to complete this topic.

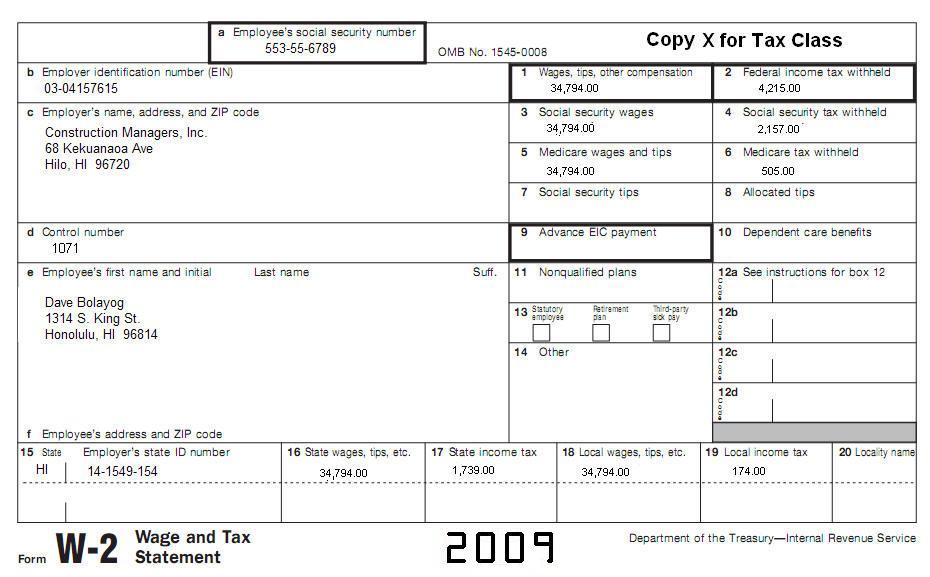

Complete a Form 2106 for Dave (553-55-6789). He is a

painter and works for a company that caters to large homes in the

community.

Then, complete a Schedule A, Form 1040.

Expenses:

Union Dues

$503.00

Tax preparation fees

$955.00

Safe deposit box at bank

$50.00 (to keep

his jewelry safe)

His total actual gas expenses

$3,200.00

Parking while at a work site

$150.00

DMV vehicle

license tax (2009 dodge)

$326.00

DMV vehicle

license tax (1993 ford pick-up)

$90.00

Gambling losses

$800.00

Costs of meals while working

late

$150.00

Check writing fees for 2009

$90.00

Speeding ticket (fine) while

driving for work

$430.00

His lunches with co-workers

while at work

$980.00 (lunch

with co-workers while talking about work improvements).

Dave had no lottery winnings

in tax year 2009.

His profession requires special white

uniforms consisting of a white

cap, white shirt (or jacket for cold weather), white bib overalls, and

white work shoes required by his union to wear on the job. The following

is the itemized list of expenses.

4 white caps with Company logo

imprinted

$25.00 each

8 white shirts with company

logo imprinted

$48.00 each

4 white bib overalls with

company logo imprinted

$46.00 each

5 painter pants not suitable

for regular use

$26.00 each

2 pairs of white Nike shoes

$75.00 each pair

Cleaning/ laundry of work

clothes

$530.00

Dave paid a total of $ 9, 600 in

rent for his 1 bedroom apartment for 2009.

Dave used his automobile (2003

Ford Pick-up) for his job and used a total of 23,000 miles for the whole

year. He started using his car car for work on January 1, 2009. His

daily roundtrip miles are about 15 per day for a total of 5,400 for the

whole year. Other miles were 2,600. He sometimes uses this pick-up

truck to help his friends when they are moving. He kept a detailed

record of his miles to and from work and his miles used at work to and

from jobs.

He has another car (2009 Dodge Ram)

that he purchased in November of 2008. He does not use this car for his

job.

In addition to his earnings from work,

Dave had the following:

Interest income from Bank

$ 672.00

Unemployment compensation

$ 125.00

Dave also had educational expenses. He

is trying to become a real estate agent. His total investment was the

following:

books and supplies

$ 370.00

registration in real estate class

$ 499.99

In addition, Dave has resume printing

and distributing costs for a total

of $ 120.00 to land him a job in his new chosen real estate

career.

Mr. Bolayog is not married and has no

children. All information on the following W-2 is current.

Tax return preparation fees

$200.

Investment seminar

$300.

Gambling losses (reported

$200 as income)

$200.

What is the

total that would be deductible by Debra on Schedule A?

A. $400.00

B. $700.00 C. $0. D. $200.00

30. If you are an

employee, you generally must complete Form 2106 (or 2106-EZ) to deduct

your travel, transportation, and entertainment expenses. Generally, you

cannot deduct travel expenses paid or incurred in connection with

A. A definite work assignment.

B. A temporary work assignment. C. An indefinite work

assignment. D. None of the above.

31. Generally, you can deduct

amounts you spend for tools used in your work if the tools

A. Wear out and are thrown away within 1 year from the date of

purchase.

B. Have a useful life beyond a year. C. Don't wear out and last for

a long time. D. None of the above.

32. You can deduct ______ of

your business-related meal expenses if you consume the meals during or

incident to any period subject to the Department of Transportation's

"hours of service" limits.

A. 20%.

B. 80%. C. 50%. D. 100%.

33. You can

deduct expenses incurred in going between your home and a temporary

work location if

A. The work location is outside the metropolitan area where you live

and normally work.

B. You have at least one regular work location (other than your home)

for the same trade or business. C. Either A or B above. D. You consider the

distance between your home and the temporary work location as this also

matters.

34. You

cannot deduct expenses incurred in going between your home and a

workplace if your home is your principal place of business for the same

trade or business.

True

False

35.

You can deduct ______ of your

business-related meal and entertainment expenses unless the expenses

meet certain exceptions.

A. 20%.

B. 80%. C. 50%. D. 100%.

36. You

cannot deduct expenses you have for education if the education is

needed to meet the minimum educational requirements to qualify you in

your trade or business, or

A. Is part of a program of study that will lead to qualifying you in a

new trade or business.

B. Is part of a program of study that will lead to complying with your

continuing educational requirements to keep your professional status

active. C. Is education needed to

advance to a higher position in your profession. D. Is education

that qualifies as long as you do not intend to enter that trade or

business.

37. A French

language teacher can deduct the cost of travel to France to maintain

his general familiarity with the French language and culture as an

educational expense.

True

False

38. The 2009

rate for business use of a vehicle is

A. 25 cents per mile.

B. 55 cents per mile. C. 35 cents per mile. D. 65 cents per

mile.

39.

Generally, you can deduct the cost of membership in any club organized

for

A. Business, pleasure, recreation, or other social purpose.

B. Conducting entertainment activities for members or their guests. C. Providing members or their

guests with access to entertainment facilities. D. None of the

above.

40. You

cannot deduct commuting expenses. If you haul tools, instruments, or

other items in your car to and from work, you can deduct

A. Only the additional cost of hauling the items, such as the rent on a

trailer to carry the items.

B. Your mileage or your actual expenses of commuting to work only for

the day that you have to haul the items. C. None of the expenses because

you have to commute to work anyways. D. You mileage or

your actual expenses everyday as long as you carry the tools or

equipment in your vehicle.

41. You can

deduct health spa expenses if there is a job requirement to stay in

excellent physical condition, such as might be required of a law

enforcement officer.

True

False

42. You apply

the 50% of your business-related meal and entertainment expenses limit

after you apply the 2%-of-adjusted-gross-income limit.