|

|

||||||||||||

| Back to Tax School Homepage | ||||||||||||

|

Topic 5 - Claiming Medical and Dental Expenses

In figuring the medical and dental expenses deduction you will learn which expenses and whose expenses you can claim on your tax return. You can include in your medical expense deduction the cost of diagnosis, cure, mitigation, treatment, or prevention of disease including the costs of equipment and devices needed for these. This topic will help you understand the itemized deduction for medical and dental expenses. Medical expenses would not include items that are for the general health as with vitamins.Student Instructions:Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

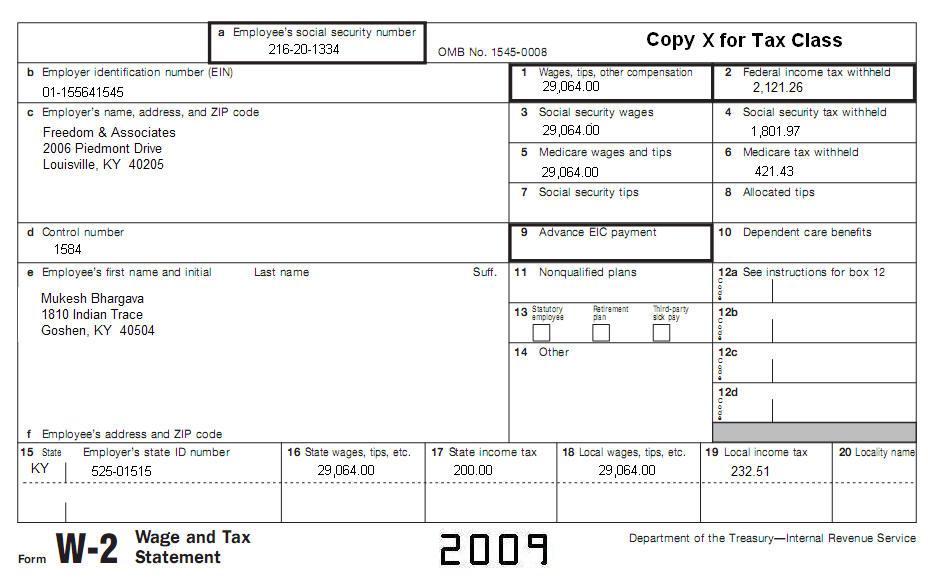

Use IRS Publication 502 to complete this topic. Complete a Schedule A for Mukesh (216-20-1334). He had the following medical expenses for the year:

Mukesh was diagnosed by his physician with a heart disease. His doctor advised Mukesh to enroll in a gym. Mukesh paid $45 per month in 2009 for the gym membership. Muskesh itemized for tax year 2008. He had un-reimbursed medical expenses for a total of $1,500 in tax year 2008. His AGI was $27,000 a bit less than his AGI in 2009 tax year. He calculated his qualified medical expenses to include in line 1 of Schedule A for 2009 tax year. In 2009, Mukesh received a reimbursement from his insurance company of the $1,500 he had paid in 2008. Get their personal information from the following W2, including address and income information.

Prepare a Federal Form 1040 for Mukesh Bhargava. Use the Schedule A that you filled out to complete the return. You may also need the Tax Table and Pub 600 Sales Tax Table.

John's medical expense deduction before the 7.5% limitation is:

A. $1,700 20. Which of the following will NOT be deductible as a medical expense?

A. The amount you pay for cosmetic surgery that is needed to correct a

scar caused from an auto accident. 21. Alice paid her mother's hospital bill. Her mother is not her dependent. Alice can deduct the hospital bill as a medical expense on her return because she paid it for a family member. True False 22. Which of the following is a medical deduction?

A. Legal abortion 23. What are deductible medical care expenses?

A. Expenses for diagnosis, cure, mitigation, treatment, or prevention

of disease. 24. You can deduct only the amount of your medical and dental expenses that is

A. More than 2% of your adjusted gross income (Form 1040, line 38). 25. You must reduce your total medical expenses for the year by all reimbursements for medical expenses that you receive from insurance or other sources during the year. If you were reimbursed for more than your medical expenses, you

A. Don't need to include the excess in income. 26. If you receive an amount in settlement of a personal injury suit, the part that is for medical expenses deducted in an earlier year is included in income in the later year if your medical deduction in the earlier year reduced your income tax in that year. True False 27. A legally adopted child is treated as your own child. This child includes a child lawfully placed with you for legal adoption. If you pay back an adoption agency or other persons for medical expenses they paid under an agreement with you, you are treated as having paid those expenses provided you clearly substantiate that the payment is directly attributable to the medical care of the child. You cannot include expenses as medical expenses

A. For care while going through the court system. 28. As a result of an accident, Thomas is required by his doctor to use a wheelchair. He arranges to have a ramp built at his front door and widens all the doorways to accommodate his wheelchair. The value of his house is not increased. The total cost of these improvements is deductible as a medical expense. True False 29. In March 2009, Phillip and Denise signed a contract with their son's dentist for braces. Jason, their son, is 9 years old and is claimed as a dependent on their return. The contract calls for a down payment in March of $200 and 12 monthly payments starting May 1st of $100 thereafter. They can deduct

A. $ 1,000 for 2009. 30. Steve had a heart ailment. On his doctor's advice, he installed an elevator in his home so that he would not have to climb stairs. The cost of the elevator was $7,000. An appraisal shows that the elevator increased the value of his home by $5,000. Steve can claim a medical deduction of

A. $2,000 31. If you and your spouse live in a community property state and file separate returns, any medical expenses paid out of community funds

A. Only the spouse that paid the medical expenses can include them. 32. You can include medical expenses you paid for an individual that would have been your dependent except that

A. He received gross income of $3,650 or more in 2009. 33. You can include in medical expenses amounts you pay for an inpatient's treatment at a therapeutic center for alcohol addiction. This does not include

A. Medical expenses amount you pay for transportation to and from AA

meetings regardless. 34. You can include in medical expenses the amounts you pay for breast reconstruction surgery if the reason is cancer. True False 35. You can include in medical expenses the amount you pay for birth control pills acquire over the counter (non-prescription). True False 36. You can include in medical expenses the cost of the following to overcome an inability to have children.

A. Procedures such as in vitro fertilization if it does not include the

temporary storage of eggs or sperm. 37. Some disabled dependent care expenses may qualify as

A. Medical expenses. 38. If you received worker's compensation, you must include the worker's compensation in income

A. Up to the amount you deducted if you did not deduct medical expenses

related to that injury. 39. If you are disabled, you can take a business deduction for expenses that are necessary for you to be able to work. If you take a business deduction for these expenses, they

A. They are subject to the 7.5% limit that applies to medical expenses.

40. If you were self-employed and had a net profit for the year, you may be able to deduct amount paid for medical and qualified long-term care insurance on behalf of yourself, your spouse, and your dependents on

A. Form 1040, line 29 as an adjustment to income. 41. If you were covered under a group health plan and you lose coverage because of a qualifying even, you should be allowed an opportunity to elect

A. The Health Coverage Tax Credit. 42. COBRA continuation coverage allows individuals who had lost their jobs to receive a reduction in health insurance premiums. True False 43. If you paid the premiums for qualified health insurance coverage, you may be able to claim the

A. The Health Coverage Tax Credit. 44. If you claim the HCTC credit, you cannot take the same expenses that you use to figure your HCTC into account in determining your

A. Medical and dental expenses on Schedule A (Form 1040). 45. The standard mileage rate allowed for operating expenses for a car when you use it for medical reasons is _________ per mile for 2009.

A. 24 cents

|

||||||||||||

| Back to Tax School Homepage |