|

|

||

| Back to Tax School Homepage | ||

|

Tax Topic 22 - Investment Income and Expenses

In this tax topic you will learn the tax treatment of investment income and expenses. You will learn what investment income is taxable and what investment expenses are deductible, including interest expenses. Here, you will learn when and how to include these items on your tax report. In addition, you will be able to determine and report gains and losses on the disposition of investment property, and property trades and tax shelters. Student Instructions:Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online Most forms are in Adobe Acrobat PDF format.

Material needed to complete the sections in this assignment:Please use IRS Publication 550 to complete this topic.

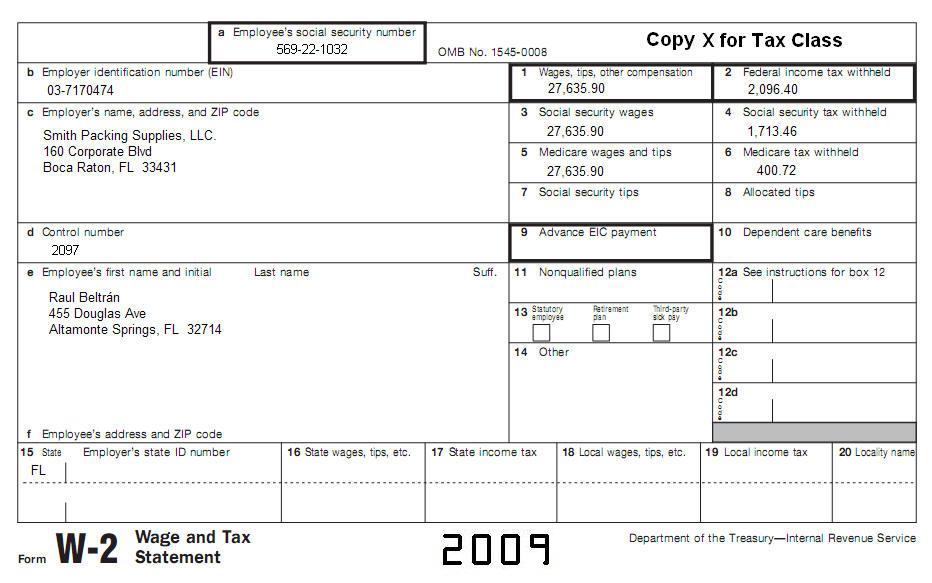

Prepare 2009 Form 1040, 2009 Form 4952, 2009 Schedule A, 2009 Schedule B. You may also need Schedule A Instructions. Raul Beltrán needs to prepare his taxes. He is an unmarried investor and has borrowed money to invest in ABC Company. The total investment interest expense from borrowed funds was a total of $14,000 for tax year 2009. Raul received the following:

Raul had no other items to itemize and he has no dependents. He paid $7,200 of rent for the entire year. All information on W-2 is current.

|

||

| Back to Tax School Homepage |