|

|

||||||||||

| Back to Tax School Homepage | ||||||||||

|

Tax Topic 7 - Tax Deductions for Interest Expense

Interest is the amount you pay for the use of borrowed money. In this topic you will learn how to claim interest expenses on your tax return. The types of interest that you can deduct are home mortgage interest, and investment interest.Student Instructions:Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

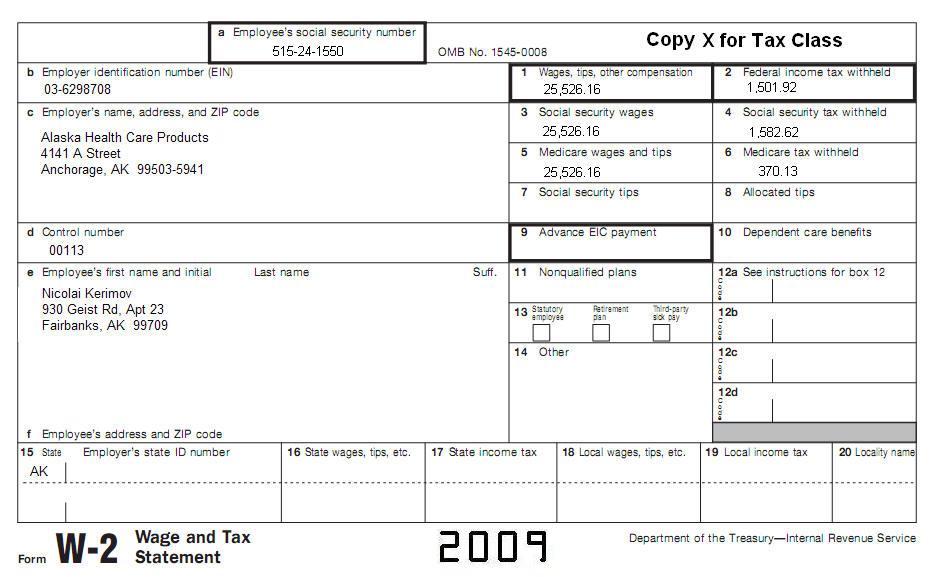

Use IRS Publication 936 and Publication 530 (mainly interest expenses but also other items) to complete this topic. Complete a Schedule A for Nicolai Kerimov (Age 24, 515-24-1550). Prepare a Federal Form 1040 for Nicolai. Get all basic information from the following W2, including income information.

He also has the following payments in 2009.

In addition to his earnings he had the following income:

Nicolai is not married and he has no children or other dependents. Nicolai paid his mortgage interest for his home to:

Remember there is no 1098 issued and that mortgage interest was paid to an individual.

|

||||||||||

| Back to Tax School Homepage |