Most forms are in Adobe Acrobat PDF format.

![]() You

will need Adobe Reader to view and print these forms. If you do not

already have Adobe Reader installed on your computer, you may

download the software for free.

You

will need Adobe Reader to view and print these forms. If you do not

already have Adobe Reader installed on your computer, you may

download the software for free.

![]()

![]()

Tax School Home Page

Student Instructions:

Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online.

Instructions to submit quiz online successfully: Step-by-Step check list

(Before you start online quiz, review the questions on this page and have your tax returns completed to be ready to answer the questions).

Most forms are in Adobe Acrobat PDF format.

![]() You

will need Adobe Reader to view and print these forms. If you do not

already have Adobe Reader installed on your computer, you may

download the software for free.

You

will need Adobe Reader to view and print these forms. If you do not

already have Adobe Reader installed on your computer, you may

download the software for free.

In this "Filing Basics" tax school part 1, we will review some tax rules that affect every person who may have to file a federal income tax return. We will cover topics such as who must and should file, what filing status and how many exemptions to use. In addition, this tax topic is about the standard deduction and taxpayers who do not itemize their deductions.

Please use the IRS Publication 501 to complete this tax assignment.

Here we will review tax rules to follow in claiming the earned income credit (EIC). The earned income credit (EIC) is a tax credit for certain people who work and have earned income. This usually means more money in your pocket and a reduction in the amount of of tax you owe.

Please use IRS Publication 596 to complete this assignment.

46. To qualify for the Earned Income Credit in tax year 2008, your investment income must not be over

A. $ 2,950

B. $ 2,850

C. $ 2,900

D. $ 2,700

47. The credit is called the Earned Income Credit because to qualify you must

A. Be at poverty level

B. Have money in your savings

C.

Work and have earned income

D. Not be living in luxury

48. If you retire on disability, benefits you receive under your employer's disability retirement plan (for EIC purposes) are

A. Always taxable

B. Unearned income

C. Not counted because disability is not taxable.

D. Considered earned income until you reach minimum retirement age

49. Income that is not earned income includes all of the following EXCEPT

A. Net earnings from self-employment

B. Earnings while an inmate in a penal institution.

C. Welfare benefits.

D. Interest and dividends.

50. To qualify for the earned income credit with a qualifying child, you must meet 3 tests which are

A.

Joint return test, age, and Residency tests.

B.

Citizenship, Age and Qualifying relative test.

C.

Relationship, Age, and Residency tests.

D.

None of the above.

51. Having a qualifying child who lives with you in your home for more than 6 months meets what test?

A. Age test

B. Relationship test

C. Residency test

D. Gross income test

52. If your Earned Income Credit was denied, send Form 8862 if it was denied because

A. You loaned your dependents to your friend.

B. You claimed a dependent that was not yours.

C. You and your spouse each tried to claim the earned income credit.

D. Any of the above.

53. Your qualifying child is your son, daughter, adopted child, grandchild, or stepchild who at the end of the year

A. Was any age if permanently and totally disabled.

B. Was under age 19.

C. Was under 24 and a student.

D. Any of the above.

54. Your son was a qualifying child of his father whom had a higher AGI. Your son lived with both parents the same amount of time and is a qualifying child for both of you. Then,

A. Your son's father can claim the credit because he had a higher AGI.

B. Both parents can claim the credit.

C. You and your child's father can decide which of you will take the EIC.

D. The one with the lower income can claim

the credit because he or she needs it most.

55. If you are a qualifying child of another person

A. You cannot claim the EIC.

B. You can claim the EIC as long as the other conditions are met.

C. You can claim the EIC if you qualify.

D. You can claim the EIC as long as you have children.

56. If your EIC for any tax year after 1996 was denied or reduced for any reason other than for a mathematical or clerical error, you must

A. Re-do your return with the correct information.

B. Not try to get the EIC credit for 5 years.

C. Attach a completed Form 8862 to your next tax return to claim the EIC.

D. Not try to get the EIC for 15 years.

57. You claimed the EIC on your 2007 tax return which you filed March 2008. In October 2008, the IRS denied your claim and determined that your error was due to reckless or intentional disregard for the EIC rules. As a result,

A. You cannot claim the earned income credit for tax year 2009.

B. You cannot claim the credit for tax years 2008 and 2009.

C. You cannot claim the credit for tax years 2009 through 2018.

D. You can't claim the credit for tax year 2019.

58. If you claimed the EIC on your 2007 tax return, which was filed in February 2008, and in December 2008, the IRS denied your claim and determined that your error was due to fraud, then

A. You can't claim the credit for tax year 2009.

B. You can't claim the credit for tax year 2008 or 2009.

C. You can't claim the EIC

for tax year 2008.

D. You can't claim the EIC

for 2008 through 2017.

59. You can receive part of your EIC in your paycheck by completing form W-5 and

A. Mailing the lower part of the form to the IRS.

B. Giving the lower part of the form to only one employer.

C. Call the IRS and explain your financial situation to a taxpayer advocate.

D. Give the form W-5 to all your employers.

60. To get part of the earned income credit paid to you throughout the year in your paycheck, you must

A. Expect to have a qualifying child.

B. Expect that your earned income and modified adjusted gross income will

be less than $35,463 ($38,583 if you expect to file 'Married Filing Jointly' for

tax year 2009).

C. Expect to be eligible for the EIC

for tax year 2009.

D. All of the above

61. What should you do if you have more than one employer and you would like to receive the advanced EIC payments?

A. Give a Form W-5 only to one employer

B. Give a Form W-5 to all of your employers

C. Send Form W-5 to the IRS

D. Fill out W-4 and claim fewer exemptions

62. If you receive advanced EIC payments in year 2008, you must

A. File a 2008 tax return only if you think they would find out.

B. File a 2008 tax return, even if you would not otherwise have to file.

C. File a 2008 tax return only if you earned enough to file.

D. File a return only if you can't determine if you have to file.

63. What is the amount of the Earned Income Credit you qualify for in tax year 2008 if you have two qualifying children and you earned $9,810 in wages and have no other income and your filing status is married Filing jointly.

A. $3,930

B. $2,917

C. $234

D. $3,910

64. In 2008, you were 24, single, and living at home with your parents. You worked and were not a student. You earned $7,500. Your parents cannot claim you as a dependent. When you file your return, you

A. Can claim the Earned Income Credit because although you are not 25 yet, no

one can claim you as a dependent.

B. Can claim the Earned Income Credit because you earned less than $12,880 and

it does not matter that you are not at least age 25.

C. Live with your parents so you don't qualify for the Earned Income Credit

because your parents will already have claimed a credit.

D. Cannot claim the Earned Income Credit because you are not at least age 25.

65. If you are 'Married Filing Jointly' and you have more than one qualifying child, to qualify for the EIC your income must be less than

A. $38,646

B. $15,880

C. $36,995

D. $41,646

66. In tax year 2008, you were age 25, single, and living at home with your parents. You earned $7,500. Your parents can't claim you as a dependent. You can claim the EIC because

A. You are not a dependent of another person.

B. You are over 25 years of age.

C. You are not using married filing separate filing status.

D. All of the above.

67. Your son is a qualifying child of both you and your son's father, because your son meets the relationship, age and residency tests for both you and your son's father. The father's AGI was more than yours. You and your son's father cannot agree on who would claim the EIC and your son lived with both of you the same amount of time during the year. Who can claim the EIC?

A. Both you and your son's father can claim the Earned Income Credit at the

same time.

B. You can claim the credit because you are the mother and that is all that

matters.

C. You can claim the Earned Income Credit as long as the child lives with you

and it does not matter if you earned less money.

D. Your son's father is able to claim the Earned Income Credit because he earned

more money.

68. You and your son lived with your mother all year. You were over 25 year of age. Your income is only $23,000 from your job. Your mother's only income is $26,000 from her job. Your child meets the relationship, age, and the residency tests for both you and your mother. If you and your mother cannot agree on who will take the EIC, then who can take the EIC?

A. Your mother because her income was higher.

B. Your mother because she is your superior.

C. Your mother because you and your son lived in her household.

D. You because the child is your son.

69. You and your sister shared a household for the entire 2008 tax year. You have five children who lived in the same household. You earned $20,000, and she earned $35,000. If you and your sister don't agree on who can claim the EIC, then your sister cannot claim the Earned Income credit because

A. You didn't sign Form 8332.

B. You are the children's parent and using the tie-breaker rule, you have the

right to not let her claim the EIC credit.

C. She earned more money and had a higher AGI and therefore she does not need

the extra money.

D. She did not care for the children as her own.

70. Earned income to meet the EIC income rules include all of the following, EXCEPT:

A. Wages, salaries, and tips.

B. Net earnings from self-employment.

C. Gross income received as a statutory employee.

D. Interest earned from your savings account.

71. U.S. Military personnel stationed outside the United States on extended active duty are not considered to have lived in the United States during that duty period for purposes of EIC rules.

True False

72. The Residency Test for purposes of the EIC rules means that the qualifying child lived only in the U.S. for more than half of the tax year. (Not to be confused with the residency test for dependents).

True False

73. Welfare benefits are considered earned income for purposes of receiving the Earned Income Credit.

True False

74. Your child can be qualifying child of another person (whom is not the father or mother) with a higher modified AGI and that person can claim the EIC if you don't agree on who will claim it.

True False

75. If you do not have a valid social security number and you write "NO" directly on 64a of Form 1040 or line 40a (Form 1040A) or line 8a (Form 1040EZ), then

A. You can claim the EIC.

B. You cannot claim the EIC.

C. You cannot send in your tax return.

D. You can claim the EIC as long as you have a valid IRS ITIN Number.

76. Social security and railroad retirement benefits are not considered earned income for purposes of the Earned Income Credit rules

True False

77. Unemployment compensation is considered earned income for EIC purposes because in order to receive unemployment compensation you are required to work.

True False

78. For Earned Income Credit purposes, the child's age does not matter if the child is permanently and totally disabled at any time during the tax year.

True False

79. Even if you have an approved Form 4029, all wages, salaries, tips and other employee compensation counts as

A. Military income

B. Unearned income

C. Earned income

D. None of the above

80. Your filing status is 'Married Filing Jointly' and you have only one qualifying child living with you for tax year 2008. Your earnings from work are a total of $33,010, and you have no other income. What is your Earned Income Credit amount?

A. $ 1,173

B. $ 634

C. $ 1,184

D. $ -0-

In this tax school part, you will learn when and when you cannot take the child and dependent care expenses credit. We will explain how to figure the credit. You may be able to claim the credit if you pay someone to care for your dependent who is under age 13 or for your spouse or dependent who is not able to care for himself or herself. To qualify, you must pay these expenses so you can work or look for work.

Please study IRS Publication 503 to complete the following questions.

81. If you pay someone to come to your home and care for your dependent or spouse,

A. You may be a household employer

B. You may have to pay employment taxes

C. You can claim the credit for child and dependent care expenses

D. Any of the above

A. Form 2441 or Schedule 2.

B. Form 2106 or Schedule 3.

C. Form 4567 or Schedule 1.

D. None of the above.

83. To qualify for child and dependent care expenses credit, you

A. Can pay for care so that you will be able to go on vacation

B. Can hire your child who is under 19 years old

C. Can hire your aunt whom you can claim as a dependent

D. Must have a child that must live with you for more than half of the year and

meet other requirements.

84. To claim the Child and Dependent Care Credit, you (and your spouse if you're married) must have earned income. Your spouse is treated as having earned income for any month that he or she is

A. A full-time student.

B. Physically not able to care for himself or herself.

C. Mentally not able to care for himself or herself.

D. Any of the above.

85. Generally, married couples must file a joint return to take the child and dependent care credit. You may be able to file a separate tax return and still take the credit if

A. You are legally separated.

B. You are living apart

from your spouse.

C. Your spouse signs an agreement not to claim the credit.

D. Both A and B above.

86. Your child and dependent care expenses must be for the care of one or more qualifying persons such as

A. A child who is under 18 years-old when the care was provided.

B. Your dependent daughter who was under the age of 13 when the care was

provided.

C. Your parents who are perfectly able to care for themselves.

D. A person who did not live with you.

87. You take your 4-year-old child to nursery school that provides lunch and a few educational activities as part of its pre-school child-care service. Which one of the following would be correct?

A. You can count the total cost as child care because the costs were partly to provide

education.

B. You can count the total cost when you figure the child and dependent care

credit because lunch and educational activities are incident to the childcare

and the cost cannot be separated.

C. Expenses were for child's lunch so they do count.

D. All of the above

88. You pay a nanny to care for your 2-year-old son and 4-year-old daughter so you can work. You become ill and miss 4 months of work but received sick pay. You continue to pay the nanny to care for the children while you are ill.

A. Your absence is not a short temporary absence, and your expenses are not

qualifying care expenses because they are not work related.

B. Your absence is a short temporary absence, and your expenses are

qualifying care expenses.

C. An absence of 6 months or less is a short, temporary absence

D. An absence of more than 2 weeks may never be considered a short,

temporary absence regardless of the circumstances.

89. You place your 12 year old child in a boarding school so you can work full-time. Which of the following would be correct?

A. You can only count the educational part of the boarding costs as

qualifying expenses

B. You can't count the boarding cost because it was not for a pre-school child

C. You can count that part of the expense in figuring your child and dependent

care credit, if it can be separated from the cost of the education

D. If you place your child in boarding school, he will be away from the home

and thus you can't claim the care credit

90. The work related expenses for the 'child and dependent care expenses care credit' are expenses that

A. Are for the cost of a babysitter while you and your spouse go out to eat.

B. Are not really for the qualifying person's care

C. Allow you to work or look for work

D. Allow you to go on vacation from work

91. If your spouse is a student or is not able to care for him or herself, he or she is treated as having earned income for any month that he or she is

A. Not your

dependent even if her or she lived in your home.

B.

A partially disabled spouse capable of caring for him or herself.

C. Physically or mentally not able to care for him or herself or is a full

time student

D. A student that is attending full time only at night

92. You can count child care expense payments you make to relatives who are

A. Not your dependents, even if they live in your home.

B. Your children who are under 19 years old, as long as they not your

dependents.

C. Your dependents for whom you (or your spouse) can claim an exemption.

D. Any of the above.

93. You, a single taxpayer, paid work related child care expenses of $3,000 in tax year 2008. You were reimbursed $2,400 by a state social services agency. Which of the following is correct regarding the child and dependent care expenses credit? (two qualifying dependents).

A. Since you were reimbursed, you can't take the child and dependent care

expenses credit

B. You can use $1,000 to figure your credit

C. You can use $600 to figure your credit

D. You can use $2,600 to figure your credit

94. If the care provider information you give is incorrect or incomplete, your credit will not be allowed unless you

A. Provide the correct information.

B. Show proof that you did pay.

C. Show due diligence in trying to supply the correct information by keeping

the care provider's completed Form W-10.

D. Call the IRS and give them the telephone number of the care provider.

95. There are many ways the taxpayer can show due diligence. Which of the following is correct as far as showing due diligence?

A. Get and keep the care provider's completed Form W-10.

B. Show a copy of the statement furnished by your employer if the the provider

is your employer's dependent care plan.

C. Show a letter or invoice from the provider if it shows the necessary

information.

D. Any of the above

96. There is a dollar limit on the amount of your work related expenses that you can use to figure the child and dependent care expenses credit. This limit is set per qualifying person. The limit is

A. $3,000 for one qualifying person.

B. $6,000 for two or more qualifying people.

C. $3,000 for each qualifying person.

D. Both A and B are correct.

97. You and your spouse (MFJ) paid $5,000 in child care, you earned $19,000 for the entire year. Your spouse did not work and was not a student or disabled. You have only one qualifying child. What is your child and dependent care expenses credit for tax year 2008?

A. $0 federal credit.

B. $990 federal credit.

C. $960 federal credit.

D. $1,600 federal credit.

98. If I am single and want to file my return and have no tax liability. If I claim the child and dependent care expenses credit for federal, would I get a refund?

A. Yes, tax liability can be zero, and you can still qualify because for

federal the

credit is refundable.

B. No, you cannot get a refund for any part of the credit that is more than

your regular tax because this tax credit is not refundable.

C. No, if you have tax, the child and dependent care credit would not cancel it and

thus there is no reason to claim it.

D. No, the federal tax system does not have a Child and Dependent Care Expenses Credit.

99. Juan and Maria Escobedo are married and keep up a home for their two pre-school children. In tax year 2008, they claimed their children as dependents. Juan earned $15,200 and Maria earned $5,100. They paid $4,900 in work related child care expenses. What is their credit?

A. $-0- for federal.

B. $501.76 for federal.

C. $1,632 for federal.

D. $1,568 for federal.

100. The amount of child and dependent care credit you can claim is limited to your regular tax.

True

False

101. In tax year 2008, if you are single with one qualifying child and your gross income is $40,100, what would your federal be if you paid $4,000 in child care?

A. $660.

B. $1,280.

C. $3,000.

D. $-0-.

102. If your qualifying person is a nonresident or resident alien who does not have and cannot get a social security number (SSN), then you are not able claim a child and dependent expenses credit for that person.

True False

103. In tax year 2008, to qualify for the federal child and dependent care credit, your adjusted gross income must be less than

A.

$70,000

B.

$43,000

C.

$100,000

D. There is no income limit.

104. You paid a fee to an agency to get the services of the nanny who cares for your 2-year-old daughter while you work. The fee you paid for the nanny search is NOT a work-related expense for the child and dependent care expenses credit.

True False

105. For purposes of claiming the Child and Dependent Care Expenses Credit, if your child turns age 13 during the year

A. The child is not a qualifying person because he has to have been under age

13

at the end of the year.

B. The child's age does not matter as long as he is your dependent.

C. The child is a qualifying person only for the qualifying expenses paid when

he or she was under age 13 for federal.

D. The child is not a qualifying child because the child has to be in pre-school.

106. In tax year 2008, Ramon's wife did not work all year because she was not able to care for herself. They are filing jointly. Ramon worked and earned $21,100. They have one qualifying child for the Child and Dependent care credit. They paid $2,000 for care of the child. How much credit can they qualify for?

A. Federal $0.

B. Federal $744.

C. Federal $640.

D. Federal $620.

107. Kevin's girlfriend claimed his son on her tax return. His son lived with her all year. Kevin paid for his child care expenses a total of $2,200. Can Kevin claim the Child and Dependent care Expenses Credit?

A. No, because he is not his dependent. Besides he did not live in his home at

all and therefore not the custodial parent.

B. Yes, because he passes the relationship test

C. Yes, because he paid for the child care expenses

D. Yes, because they (Kevin and his girlfriend) signed Form 8332

108. If you are the non-custodial parent, for purposes of claiming the child and and dependent care credit, the child can be your qualifying child.

True

False

109. If you and your qualifying person did not live in the same home for more than half of the year, other than for reasons because of birth, death or temporary absences, you are able to claim the child and dependent care expenses credit.

True

False

110. For purposes of the child and dependent care expenses credit, if your spouse was permanently and totally disabled and you have two qualifying children he or she is considered to have earned $500 per month for the time that he or she was disabled.

True False

In this tax school part, you will be able to review your tax knowledge you have in tax preparation. You will be able to apply knowledge you have integrated with new knowledge.

Use publication IRS Publication 17 to complete this topic.

IRS Form 8812

IRS Form 8863

IRS Form 4137

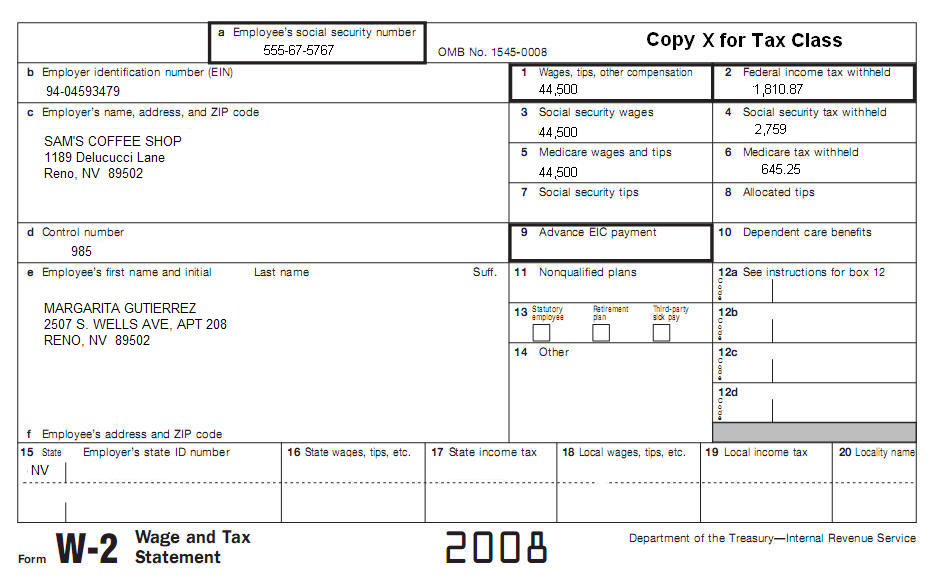

Prepare the appropriate Federal forms for Margarita Gutierrez. Her address is current on Form W-2. Get all her basic information from the following W2, including income information.

Margarita (DOB 09/10/1966) is a divorced woman. For tax year 2008 she received the following:

| Unemployment Compensation $ 985 | |

| Interest from First Bank $414 | |

| Lottery winnings: $ 911 |

Margarita has three children:

| Carlos Tovar, DOB August 6, 2002 (SSN 555-76-7755) | |

| Anita Tovar, DOB September 15, 2001 (SSN 555-76-7754) | |

| Javier Tovar, DOB December 31, 1991 (SSN 555-76-7753) |

Margarita paid rent $8,800 for tax year 2008.

March 12, 2008, Margarita placed a deposit of $180 ($90 for each child) with a care provider to reserve a place for her two children Carlos and Anita in the child care facility. Her plans were for the facility to care for her children until her mother suggested that it would be great for her (Margarita's mother) to take of the children. As a result, Margarita forfeited her deposit.

In 2008, Margarita paid her mother Linda Gutierrez $ 2,100 ($1,050 for each child) for child care. Linda lives at 1965 S. Virginia St., Reno, NV 89502. Her number is 912-52-1060. Linda cared for both children.

Margarita is the only person that can claim the children. The children lived with her for all of 2008 tax year. She paid all of the household expenses and she was the only person supporting her children.

Margarita's son Javier turned 17 on December 31, 2008. He is a U.S. Citizen and Margarita can claim him as a dependent. Margarita was told by another preparer that she can get the child tax credit for Javier because Javier was 16 years old for the most part of the tax year.

In 2008, Margarita bought a new car for $ 9,000 cash and received a $ 400 rebate check from the manufacturer.

Margarita received $ 3,000 in court ordered alimony payments from her ex-husband Francisco Tovar (SSN 540-16-7021) as specified in her divorce decree .

In 2008, Margarita makes a payment directly to an eligible educational institution for her son Javier's qualified educational expenses. She paid $ 2,000 for him on borrowed funds. These funds will be paid with a balloon payment at the end of 2009. Margarita is asking if she can take both the Hope credit and the Lifetime Learning Credits. Margarita will claim both credits if she can.

Margarita received tip income that she did not report because according to her employer she was not supposed to report tips for certain months that the amount did not reach a minimum reportable amount. Her employer included in Margarita's W-2 only tips that were more than the minimum amount to report. I asked Margarita to bring me just the totals of the tip income she received per month. The following list shows her tips received in their respective months.

Margarita will contribute the most that she can contributed to a traditional IRA on April 10, 2009 a few days before her return is due to be filed. She was not covered by a retirement plan at work.

111. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 7?

A. $ 46,326.

B. $ 44,500.

C. $ 44,606.

D.

None of the above.

112. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 11?

A. $ 985.

B. $ 3,000.

C. $ -0-.

D.

None of the above.

113. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 19?

A. $ 985.

B. $ 911.

C. $ -0-.

D.

None of the above.

114. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 21?

A. $ 985.

B. $ 911.

C. $ -0-.

D.

None of the above.

115. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 22?

A. $ 46,326.

B. $ 44,500.

C. $ 49,916.

D.

None of the above.

116. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 32?

A. $ 5,000.

B. $ 4,000.

C. $ -0-.

D.

$ 3,000.

117. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 48?

A. $ 181.

B. $ 2,100.

C. $ 420.

D.

None of the above.

118. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 50?

A. $ 1,600.

B. $ 400.

C. $ 2,000.

D.

None of the above.

119. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 52?

A. $ 3,000.

B. $ 2,000.

C. $ 1,970.

D.

$ 846.

120. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 66?

A. $ 859.

B. $ 1,141.

C. $ 1,154.

D.

$ 4,928.

121. Look at the Form 1040 you prepared for Margarita. What is the amount on Form 1040, Line 73a?

A. $ 3,400.

B. $ 1,811.

C. $ 2,670.

D.

$ 2,965.

122. To claim the child tax credit, you can claim it on Form 1040EZ.

True False

123. Your son turned 17 on December 31, 2008. You claim him as a dependent on your return. What is the amount of your child tax credit.

A. $ 1,000.

B. $ 2,000.

C. $ 3,000.

D. $

-0-.

124. Credits, such as the child tax credit, the adoption credit, or the credit for child and dependent care expenses, are used to reduce tax. If your tax on Form 1040, line 46, or Form 1040A, line 28 is zero, figure the child tax credit to see if you qualify.

True False

125. The additional child tax credit is a credit you may be able to take if you are not able to claim the full amount of the child tax credit.

True False

126. This credit is called the "Earned Income Credit" because, to qualify, you must work and have earned income. Earned income includes

A. Certain dependent care benefits.

B. Certain adoption benefits.

C. Net earnings from self-employment or gross income received as a statutory

employee.

D.

All of the above.

127. You can elect to include your non-taxable combat pay as earned income to figure the earned income credit.

True False

128. For the Earned Income Credit, payments you received from a disability insurance policy that you paid the premiums for are earned income once you have reached minimum retirement age.

True False

129. During the 2008 fall semester, Luis was a high school student who took classes on a half-time basis at Los Felix College. Luis was not enrolled as part of a college degree program at Los Felix College because this college only admits students to a degree program if the students have a high school diploma or equivalent. Luis

A. Did not have expenses that qualify him to figure a hope credit.

B. Was an eligible student for the hope credit for tax year 2008.

C. Was not an eligible student for the hope credit for tax year 2008.

D.

None of the above.

130. Generally, you can claim an educational credit if you

A. Pay qualified education expenses of higher education.

B. Pay the education expenses for an eligible student.

C. Pay qualified education expenses for your spouse, or a dependent for whom you

claim an exemption on your return.

D.

All of the above.

131. Include in your income on Form 1040, line 11, any alimony payments you received.

True False

132. Report the value of any non-cash tips, such as tickets or passes, to your employer, because you have to pay social security and Medicare taxes or railroad retirement tax on these tips.

True False

133. If you received $20 or more in cash and charge tips in a month from any one job and did not report all those tips to your employer, you must report the social security and Medicare taxes on the un-reported tips as additional tax on your return. To figure the additional taxes use

A. Form 8880.

B. Form W-2.

C. Form 4137.

D.

Form 8919.

134. You can set up and make contributions to a traditional IRA if

A. You (or, if you file a joint return, your spouse) received taxable

compensation during the year.

B. You were not age 70 1/2 by the end of the year.

C. You have a job and your employer agrees to you making a contribution.

D.

Both A and B are correct.

135. To claim the child tax credit your qualifying child must be

A. Under age 17 by the end of tax year 2008.

B. Your child, stepchild, grandchild, great-grandchild.

C. An eligible foster child that lived with you for more than half of 2008.

D. All of the above

136. If the child tax credit exceeds the tax liability, part or all of the excess may be refundable as an additional credit calculated on Form 8812.

True False

137. For purposes of the Child Tax Credit, your modified AGI is your AGI plus

A. Any amount excluded from income because of the exclusion of income from

Puerto Rico.

B. Any amount on line 45 or line 50 of Form 2555.

C. Any amount on line 18 of Form 2555-EZ or line 15 of Form 4563.

D. Any of the above

138. For tax year 2008, how much Is the maximum child tax credit amount per qualifying child?

A. $600

B. $2,600

C. $1,000

D. $2,000

139. Juanita Ramos is a single woman whom has three dependent children living with her. Her children are under 17. Juanita's total income is $25,000 as shown on her W-2. Her social security and Medicare taxes from Forms W-2, boxes 4 and 6 show $1,913 total withheld. Juanita provided her children total support and they lived with her all year. No one else can claim an exemption for Juanita or the children. Other than the Earned Income Credit, she had no other credits. Figure out what the Additional Child Tax Credit is for tax year 2008.

A. $ 303

B. $ 2,697

C. $ 2,475

D.

$ -0-

140. Albert has one child who turned 17 years old on December 10, 2008. Albert's tax liability on Form 1040, line 46 is $1,100. What is Albert's Additional Child Tax Credit amount for 2008?

A. $ 1,000

B. $ 100

C. $ -0-

D.

None of the above.

![]()