|

|

||||||||||||||

|

Tax Lesson 6 - Claiming Medical and Dental Expenses

|

||||||||||||||

This topic will help you understand the itemized deduction for medical and dental expenses. In figuring this deduction you will learn which expenses and whose expenses you can claim on your tax return. You can include in your medical expense deduction the cost of diagnosis, cure, mitigation, treatment, or prevention of disease including the costs of equipment and devices needed for these. Medical expenses would not include items that are for the general health as with vitamins.Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list

Most forms are in Adobe Acrobat PDF format.

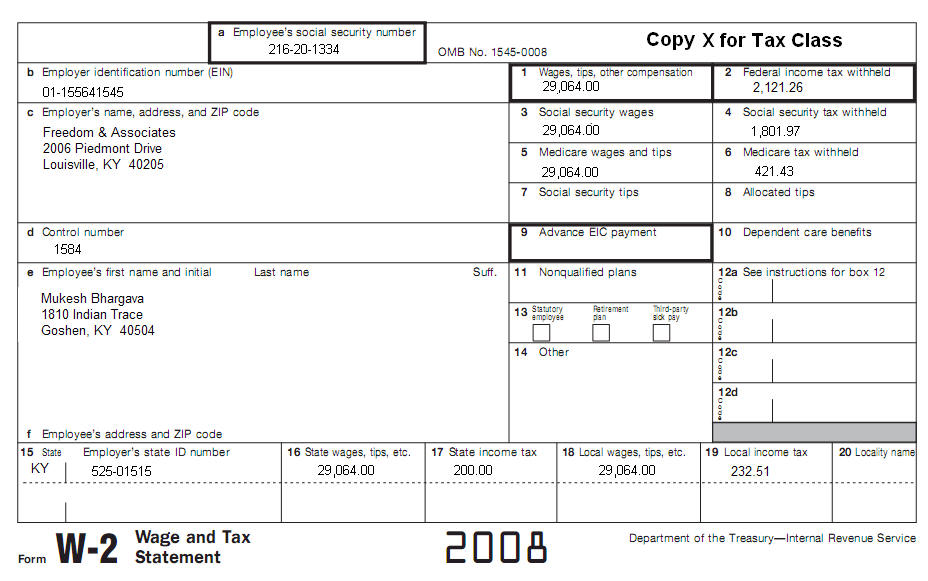

Use IRS Publication 502 to complete this topic. Complete a Schedule A for Mukesh (216-20-1334) and Sarita Bhargava (342-06-1213). Sarita did not work. They had the following medical expenses for the year:

Mukesh was diagnosed by his physician with a heart disease. His doctor advised Mukesh to enroll in a gym. Mukesh paid $45 per month in 2008 for the gym membership. Fill in Schedule A (Form 1040) line 5 using state and local tax amounts deducted on Form W-2. Get their personal information from the following W2, including address and income information.

Prepare a Federal Form 1040 for Mukesh Bhargava. Use the Schedule A that you filled out to complete the return.

John's medical expense deduction before limitation is:

A. $1,700

20. Which of the following will NOT be deductible as a medical expense?

A. The amount you pay for cosmetic surgery that is needed to correct a scar

caused from an auto accident.

|

||||||||||||||

|

Copyright © 2017 [Hera's Income Tax School]. All rights reserved. Revised: 11/21/17 |