|

|

||||||||||||||||||||||||||||||

|

Tax Lesson 31 - Moving Expenses

|

||||||||||||||||||||||||||||||

In this tax topic you will the learn how to take a deduction for certain expenses of moving to a new home because of a change in job location or starting a new job. You will become aware of what moving expenses are deductible and not deductible, who can take the moving expense deduction, when and where to report the expenses and how reimbursements affect your moving expenses deduction. Moving expense deductions can be deducted by either employees or self employed taxpayers.Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

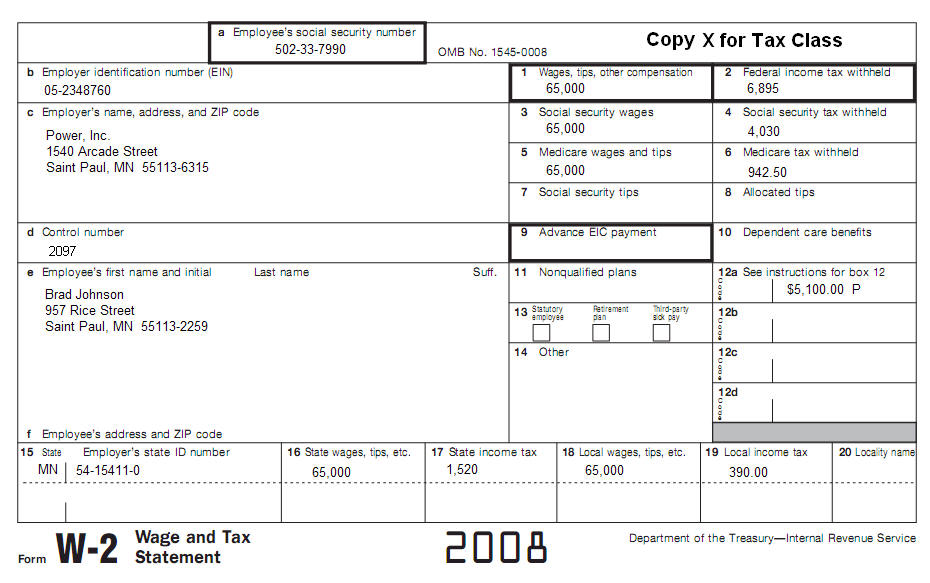

Use IRS Publication 521 to complete this topic. Prepare Form 1040, Form 3903 and California Form 540 . Brad Johnson is married and has no children. He owned his home in Florida where he worked. On December 8, 2007, his employer told him that he would be transferred to Saint Paul as of January 20, 2008. His wife, Samantha (SSN 610-25-3940), flew to Saint Paul on January 2008 to look for a new home. She put a down payment of $25,000 on a house being built and came back to Florida on January 8, 2008. The Johnsons sold their Florida home for $1,500 less than they paid for it. The home was free and clear by the time the construction was completed. They contracted to have their personal effects moved to Saint Paul on January 15, 2008. The family arrived in Saint Paul January 18, 2008 only to find out that their new home was not yet completed. They stayed in a nearby motel awaiting completion of the house until February 12, 2008. On January 20, 2008, Brad went to work in the Saint Paul plant where he works to the present time. Their records for the move show: 1). Samantha's pre-move house hunting trip:

2). Down payment on Saint Paul home.......$25,000. 3). Real estate commission paid on sale

4). Loss on sale of Florida home (not

5). Amount paid for storing and moving personal

6). Expenses of driving to Saint Paul:

7). Cost of temporary living expenses in Saint Paul:

Brad was reimbursed $5,749 under an accountable plan as follows:

The employer included this reimbursement on Brad's Form W-2 for the year. The reimbursement of deductible expenses, $5,100 for moving household goods and travel to Saint Paul, was included in Box 12 of Form W-2. His employer identified this amount with code P. The employer included the balance, $649 reimbursement of nondeductible expenses, in box 1 of W-2 with Brad's other wages. The employer withholds taxes from the $649 which is also included in W-2.

|

||||||||||||||||||||||||||||||

| Back to Tax School Homepage |