|

|

|

Tax Lesson 3 - Tax Exemptions

|

|

This tax topic will help you learn about tax exemptions, when you

can claim them and who are the qualifying individuals you can claim on your tax

return. You usually can claim exemptions for yourself, your spouse, and each

person you can claim as a dependent.

Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

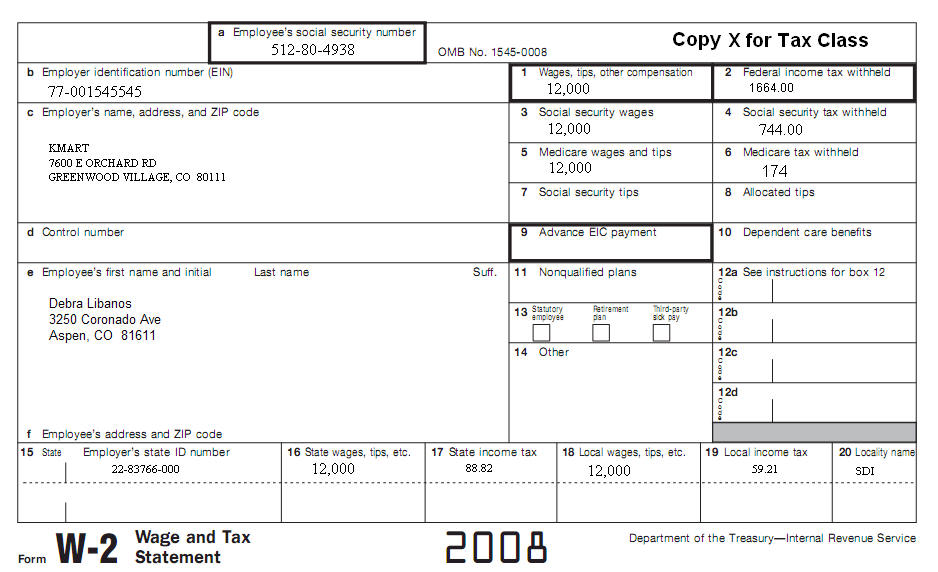

Please use IRS Publication 501 to answer the questions from the following quiz. Complete a return for Debra Libanos. Get all their basic information from the following W2, including income information. Complete Form 1040A (1040A Instructions). Use the following attached W2, information on W2 is current.

Debra has her niece Tsehay Adaba, (D.O.B. born 8-23-2001 and SSN 610-04-1090) whom she would like to claim on her tax return. Tsehey didn't live with Debra. However, Debra provided more than half of Tsehay's support. No one else can claim Tsehay or Debra as a dependent.

|

| Back to Tax School Homepage |