|

|

||||||||||||

|

Tax Lesson 26 - Selling Your Home

|

||||||||||||

|

In this topic your will become familiar with the rules that apply

when you sell your main home. Your main home is the home lived in most of the

time. You will learn the amount that you can exclude from income of the gain

from the sale of your home. In addition, you will learn what to do when the sale

cannot be excluded from income, in which case it becomes fully taxable. You will

also learn what to do with a non-deductible loss of the sale of your home.

Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

Use IRS Publication 523 and

Form 1040 Instructions to

complete this topic.

Prepare Form 1040 and Schedule D.

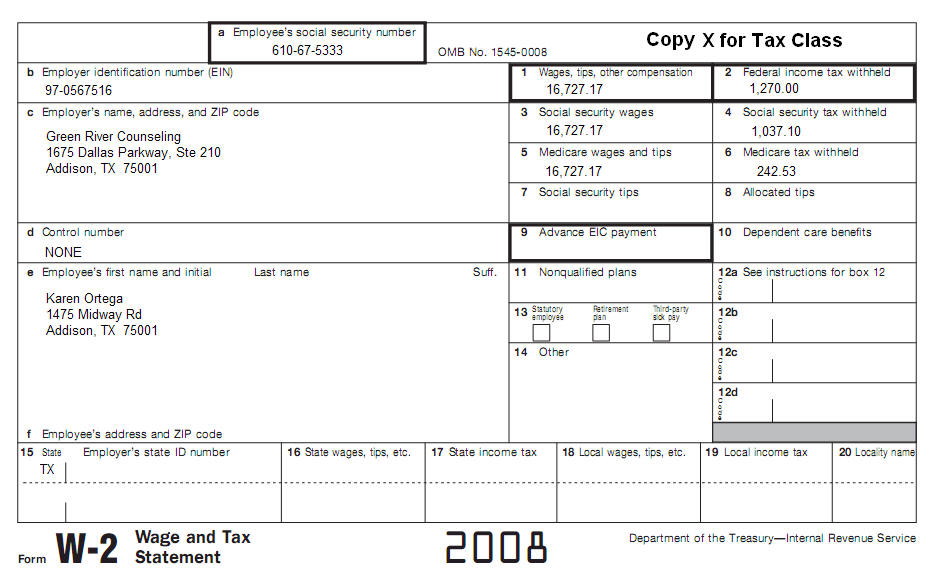

Karen (Age 24), a single person, bought her home February 23, 1997. She lived in the home until May 31, 2006, when she moved out of the house and put it up for rent. Karen rented her home until May 31, 2007. That's when she moved back into the house and lived there until she sold it on January 10, 2008. Karen wants to exclude all of the gain from the sale of her home. Karen's records show the following:

Karen's W-2 shows her current address information.

|

||||||||||||

| Back to Tax School Homepage |