|

|

||||||||||||||||||||||

|

Tax Lesson 24 - Residential Rental Income and Expenses

|

||||||||||||||||||||||

|

In this tax topic you will learn how to report rental income

and expenses on tax returns, the expenses you are allowed to deduct. Amongst the

items you will become aware of here, are the rental-for-profit activities in

which there is no personal use of the property. In addition, you will learn

about taking depreciation as it applies to rentals and how to claim the correct

amount. Finally, you will also become aware of the rules for rental income and

expenses when there is also personal use of the property, such as with vacation

homes.

Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

Use IRS Publication 527 to complete this topic. Prepare Form 1040, Form 4562, Schedule A, Schedule E. Teresa is single and has no children. In August, 2008, Teresa moved in with her mother to keep her company. Instead of selling the condo she had been living in, she decided to convert it to rental property. Teresa selected her tenant and started renting the condo on September 1st. Teresa charges $800 per month for rent and collects it herself. Teresa received an $800 security deposit and $800 last months rent from her tenant. She plans to return the security deposit to her tenant at the end of the lease but not until doing an inspection on the condition of the condo. She actively participated in the rental activities. She had advertised and rented the condo to the current tenant herself. She also collected the rents. All repairs were contracted by Teresa. Her condo expenses for the 2008 tax year are:

Teresa bought this property in 1984 for $35,000. Her property tax was based on assessed values of $10,000 for the land and $25,000 for the condo. Before changing it to rental property, Teresa added several improvements to the condo. She figures her adjusted basis as follows: Improvements...............................Cost

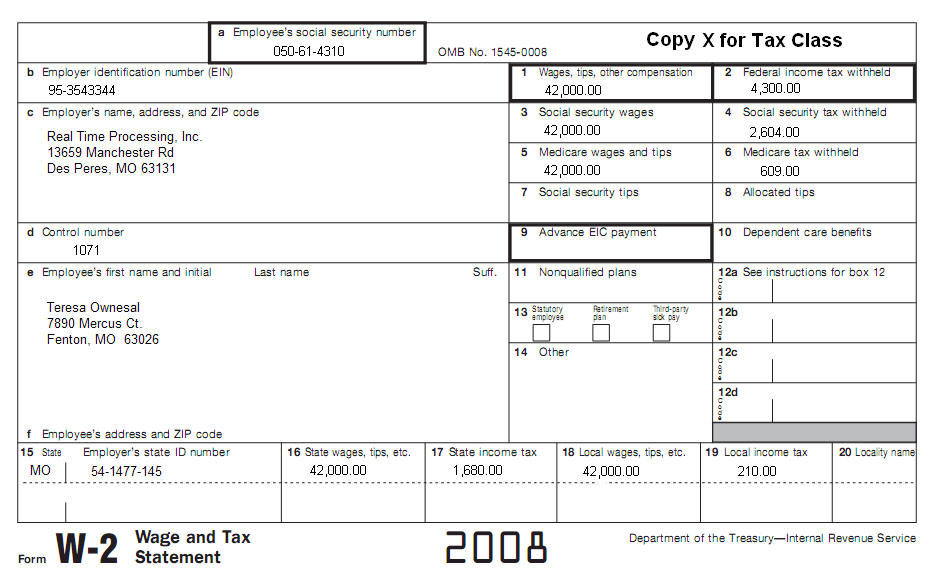

On September 1, 2008, when Teresa changed her 1 bedroom condo to rental property. The property had a fair market value of $92,000 ($20,000 land and $72,000 building). Property is located at 6109 Sunnyslope Drive, Kansas City, Missouri, 64134. All her information on the W-2 is current, including address information.

|

||||||||||||||||||||||

| Back to Tax School Homepage |