|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Tax Lesson 20 - Self-Employment Income and Tax

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

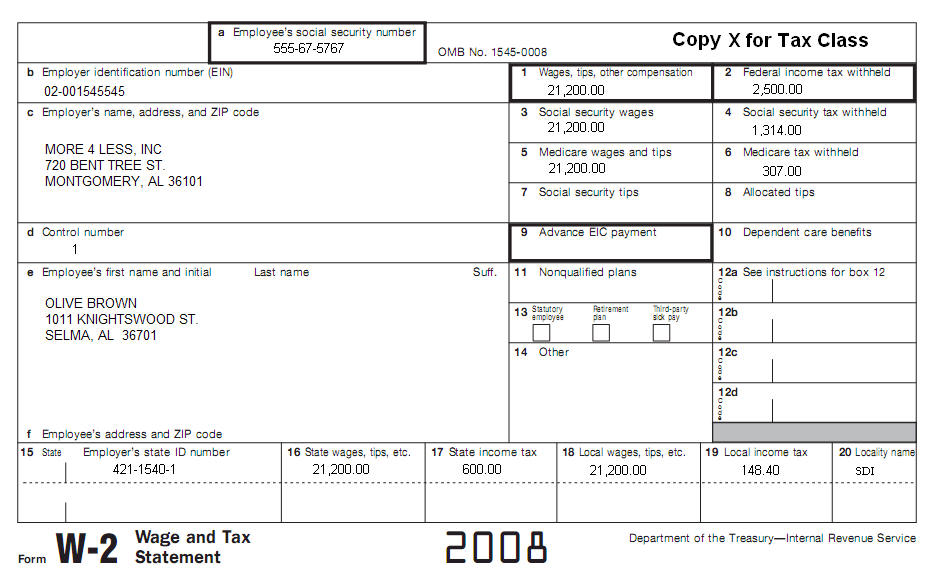

In this tax topic you will learn the federal tax laws that apply to small business sole proprietors and to statutory employees. Here, you will be introduced to business income, business expenses and certain business tax credits to use in filing your business return. How do you know when you are self-employed? You are self-employed if you carry on a trade or business as a sole proprietor or as an independent contractor. In addition, in this topic you will be introduced to self-employment (SE) tax and you will learn how to figure the SE tax.Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online You may need acrobat reader to download forms and publications online.Use IRS Publication 334, Schedule F instructions to complete this topic. Please complete a return for Olive Brown. Prepare Form 1040, Schedule C , Schedule SE, Form 4562. Olive is a 27 year old unmarried taxpayer. She owns and manages Fashions At Discount (Activity codes). A Clothing store that she started in 2008. Address for business is 2304 Cobbs Ford Rd, Selma, AL 36701. She had the following for her store: Income Statement Year Ended December 31, 2008

Cost of Goods Sold

Expenses:

Inventory is valued at cost and there was no change in determining inventory at any time during the year. In addition, Olive had the following:

Olive paid rent all year in 2008. Use W2 for basic information. Address and other information on W2 is current.

Answer the following questions as accurately as possible.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Back to Tax School Homepage |