|

|

|

Tax Lesson 18 - Social Security and Equivalent Railroad Retirement Benefits

|

|

In this topic you will learn the federal income tax rules for

social security benefits and equivalent railroad retirement benefits. After

completing this topic you should be able to know how to figure whether your

benefits are taxable by using the social security benefits worksheet. In

addition, you will know how to report your taxable benefits and how to treat

repayments that are more than the benefits your receive during the tax year.

Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

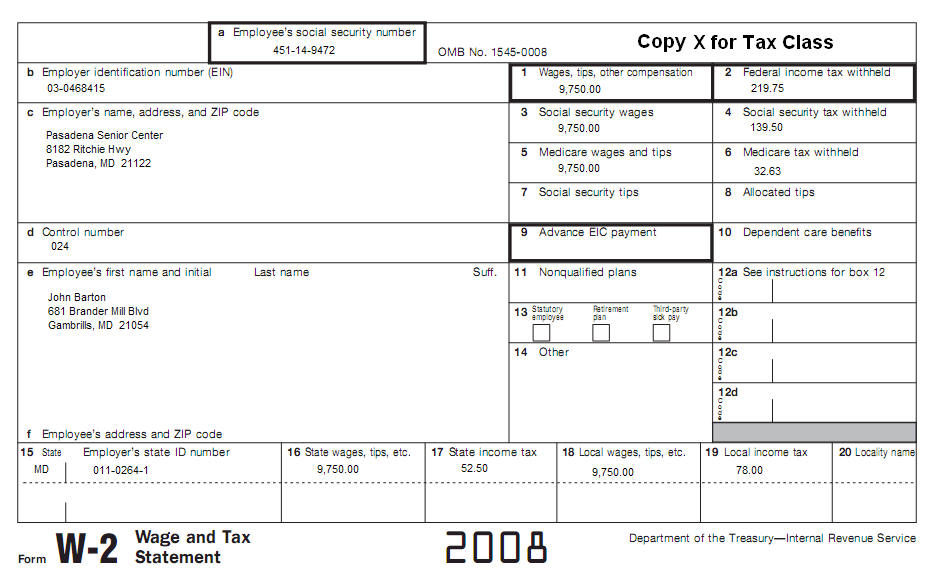

Use IRS Publication 915 to complete this topic. Prepare a Federal Form 1040A for John Barton. Address information on Form SSA-1099 is current. Mr. Barton received Social Security benefits. In addition to the income receive from his part time job and his Social security benefits, Mr. Barton receive $4,000 interest income from his bank. Mr. Watson's date of birth is August 20, 1944.

|

| Back to Tax School Homepage |