|

|

||

| Back to Tax School Homepage | ||

|

Topic 25 - Divorced or Separated Individuals

In this tax topic you will learn the tax rules that apply to divorced or separated individuals. In this topic you will also cover general filing information and even more information on filing status and exemptions you are entitled to claim when you are divorced or separated. In addition, you will learn about payments and transfers of property that occur as a result of divorce such as alimony and how you must report them on the tax return. Finally, your will become familiar with the deductions allowed for some of the costs of obtaining a divorce. Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

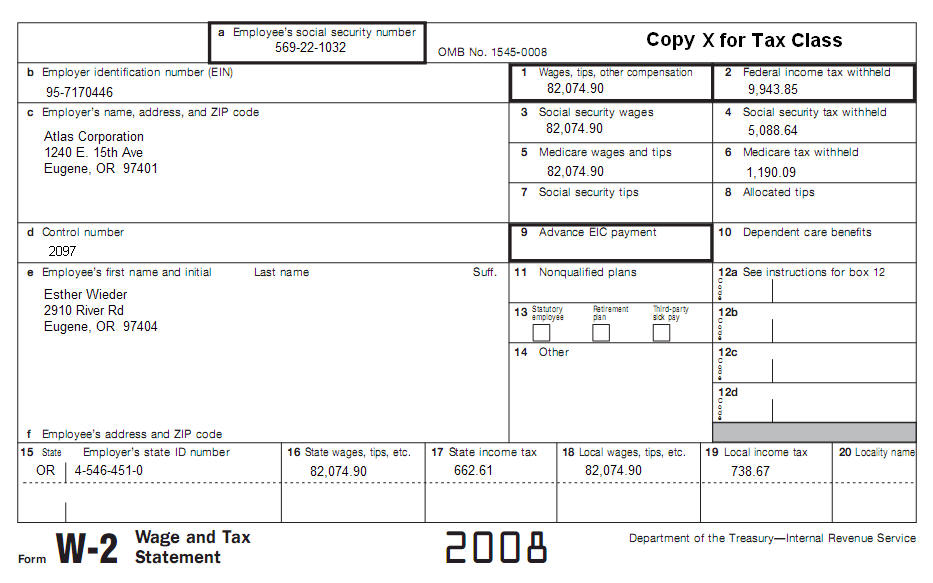

Use IRS Publication 504 to complete this topic. Prepare Form 1040 and Schedule A. Esther must pay her former husband or his estate $20,000 in cash each year for 10 years. The death of her former spouse would not terminate these payments under state law. Laura's former spouse's name is Melvin Davis (SSN 570-88-9521). Esther does not have any children and she remains divorced. Esther made the following estimated payments:

Use the following information and Form W-2 to complete return. There is no other information.

|

||

| Back to Tax School Homepage |