|

|

|

Topic 13 - Earned Income Credit

|

|

This tax topic will teach you the rules and regulations regarding

claiming the earned income credit. The earned income credit (EIC) is a tax

credit for certain people who work and have earned income. A tax credit usually

reduces the amount owed and may give you a refund even if you have had no money

withheld or have made no estimated tax payments along the year.

Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

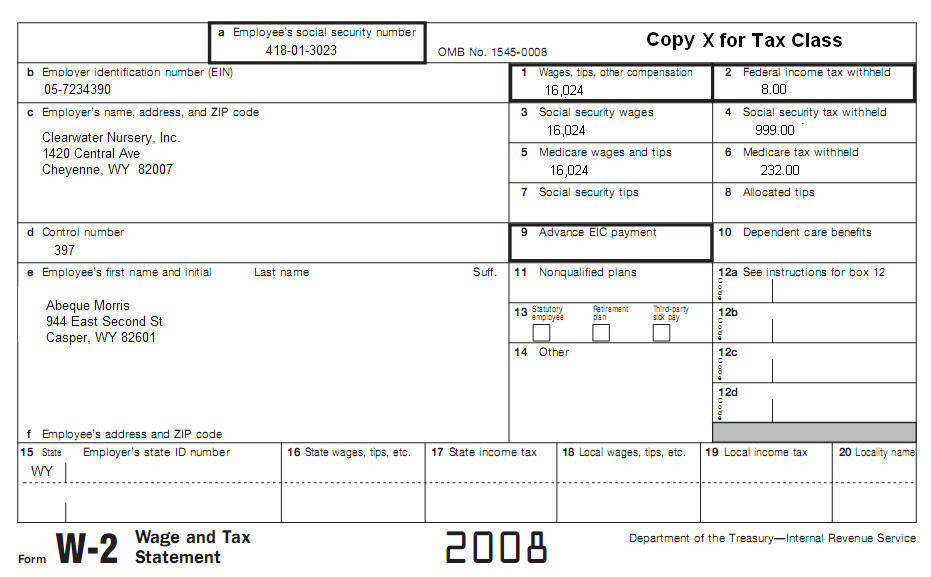

Use IRS Publication 596 to complete this topic. Complete a tax return for Abeque Morris. Her Children who lived with her all year are: Son: James Gowdy.....(626-12-6525) DOB 4-17-1997 Daughter: Nellie Gowdy....(688-54-5661) DOB 6-18-1995 Abeque was single and was the only person that supported her family in 2008. she also received Interest income from her bank account $390. Complete Form 1040A and Schedule EIC (Form 1040) using the following W2 information. All information on W2 is current, including address information.

B. $ 2,700 or Less. C. $ 2,800 or Less. D. $ 2,950 or Less. 23. Earned income includes the following income.

A.

Wages, salaries, tips, and other taxable employee pay.

24. Oscar, age 26, is a single taxpayer who had earned income of $9,200 in 2008. His investment income was $200. He had no other income and is not the dependent or qualifying child of another person. Assuming he meets all the other requirements, Oscar

A. Does not qualify for the earned income credit.

25. You have only two qualifying children living with you in tax year 2008 and are not married. Your earnings from work are a total of $28,210, and you have no other income. Assuming you meet all the requirements, what is your Earned Income Credit amount?

A. $ 802.

26. Your son is a qualifying child of both you and your brother, because he meets the relationship, age and residency tests for both of you. Your brother's AGI was more than yours. Under the tie-breaker rule, if you both don't agree on who will take the EIC, then

A. Both you and your brother can claim the Earned Income Credit at the

same time. 27. If you received advanced EIC payments in year 2008, you must

A. File a 2008 tax return only if you think they would find out.

28. You can choose to include combat pay in your earned income for purposes of computing this credit. If you are married,

A. Each of you can make this election separately. 29. If your EIC for any year after 1996 was denied and it was determined that your error was due to reckless or intentional disregard of the EIC rules, then you cannot claim the EIC for the next 2 years. If your error was due to fraud, then

A.

You cannot claim the EIC for the

next 5 years. 30. Items that are considered non-earned income for Earned Income Credit purposes include interest and dividends, pensions and annuities, social security and railroad retirement benefits (including disability benefits), alimony and child support and

A. Welfare benefits. |

| Back to Tax School Homepage |