|

|

||||||||||||||||||||||||||||||||||||||||||||||||||

|

Topic 11 - Tax Deduction for Job Expenses and other items

|

||||||||||||||||||||||||||||||||||||||||||||||||||

|

In this topic you will learn which expenses you can claim as

miscellaneous itemized deductions. You will cover which expenses are subject to

the 2% limit and which expenses are not. You will also learn which expenses you

cannot deduct and how to report the expenses that are deductible. For example,

some of the expenses that are deductible are unreimbursed employee expenses that

are incurred during the year and that are ordinary and necessary.

Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

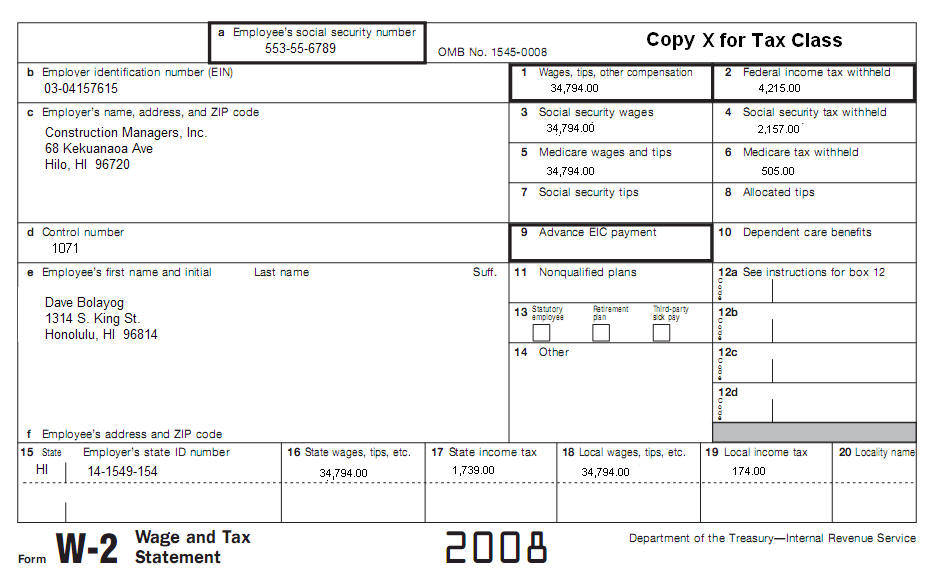

Use IRS Publication 529 to complete this topic. Complete a Form 2106 for Dave (553-55-6789). He is a painter and works for a company that caters to large homes in the community. Then, complete a Schedule A, Form 1040. Expenses:

*According to his gambling diary, Dave had a total of $800 in gambling losses. He had no winnings in tax year 2008. His profession requires special white uniforms consisting of a white cap, white shirt (or jacket for cold weather), white bib overalls, and white work shoes required by his union to wear on the job. The following is the itemized list of expenses.

Dave paid a total of $ 9, 600 in rent for his 1 bedroom apartment for 2008. Dave used his automobile (2002 Ford Pick-up) for his job and used a total of 23,000 miles for the whole year. He started using his car car for work on January 1, 2008. His daily roundtrip miles are about 15 per day for a total of 5,400 for the whole year. Other miles were 2,600. He totaled 15,000 miles that were qualified work related miles. 7,500 miles from January 1, 2008 through June 30, 2008 and 7,500 miles from July 1, 2008 through December 31, 2008. He sometimes uses this pick-up truck to help his friends when they are moving. He kept a detailed record of his miles to and from work and his miles used at work to and from jobs. He has another car (2008 Dodge Ram) that he purchased in November of 2007. He does not use this car for his job. In addition to his earnings from work, Dave had the following:

Dave also had educational expenses. He is trying to become a real estate agent. His total investment was the following:

In addition, Dave has resume printing and distributing costs for a total of $ 120.00 to land him a job in his new chosen real estate career. Mr. Bolayog is not married and has no children. All information on the following W-2 is current.

What is the total that would be deductible by Debra on Schedule A?

A.

$400.00 30. If you are an employee, you generally must complete Form 2106 (or 2106-EZ) to deduct your travel, transportation, and entertainment expenses. Generally, you cannot deduct travel expenses paid or incurred in connection with

A. A definite work assignment.

|

||||||||||||||||||||||||||||||||||||||||||||||||||

| Back to Tax School Homepage |