|

||||

|

1. Federal Tax Updates |

||||

|

Table of Contents |

||||

|

Tax changes New individual and capital gains tax rates What’s happening for 2018 tax returns? What is a capital asset? Increase in the Standard deduction and change in filing requirements for each filing status Temporary reduction of personal exemption to zero Adjustments to Income Alimony Moving expenses Roth IRA recharacterization rules Schedule C Provisions Elimination of entertainment expenses New Section 179 expense limits 100% expending (Bonus Depreciation) Luxury auto limits Itemized Deductions Schedule A Medical expenses State and local tax deduction and limit Home mortgage interest deduction changes Charitable contribution changes AGI limit for cash contributions No deduction for athletic tickets Repeal of exception to contemporaneous written acknowledgement Casualty and Theft loss deduction limited to only federally declared disaster areas.Suspension of miscellaneous itemized deductions subject to 2% of AGI Suspension of overall limitation on itemized deductions Credits Enhanced Child Tax Credit CTC Increase in amount to $2,000 CTC phase-out and refundable/nonrefundable amounts SSN Requirement New $500 nonrefundable credit for dependents other than a qualifying child or for a qualifying child without the required SSN Alternative Minimum Tax (AMT 20% deduction for a pass through qualified trade or business Kiddie Tax modifications Section 529 Plan changes Achieving a Better Life Experience (ABLE) account changes Discharge of certain student loan indebtedness from 2018 through 2025 Net Operating Loss (NOL) changes Affordable Care Act (ACA) provisions 2018 requirement for individual insurance and Shared Responsibility payment Individual Mandate Penalty - eliminated for 2019 Changes in employee fringe benefits Real property depreciation

|

||||

|

1. Federal Tax Updates |

||||

| Tax changes | ||||

|

The new tax reform was finally approved by Congress on December 22, 2017. On December 22, 2017, the Tax Cuts and Jobs Act was passed by Congress. This new tax act provided reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018”. This legislation, which the President signed into law on Dec. 22, 2017, is the most sweeping tax reform measure in over 30 years. The new legislation makes fundamental changes to the Internal Revenue Code that will completely change the way individuals and businesses calculate their federal income tax liability, so as to create numerous planning opportunities. The changes affecting individuals include new tax rates and brackets, an increased standard deduction, elimination of personal exemptions, new limits on itemized deductions (state taxes, mortgage interest), and the repeal of the individual mandate under the Affordable Care Act. The changes affecting businesses include a reduction in the corporate tax rate, increased expensing and bonus depreciation, limits on the deduction for business interest, and a new 20% deduction for pass-through business income. The foreign provisions include an exemption from U.S. tax for certain foreign income and the deemed repatriation of off-shore income. This new tax reform is the new Tax Cuts and Jobs Act (TCJA). This new tax reform was passed to take effect on both individuals and businesses. This new legislature dictates how businesses compute business interest and what business interest limitations exist under the new legislation recently passed on December 22, 2017. This new tax law will also affect the withholding on the transfer of non-publicly traded partnership interests and tax withholding me need adjustment for certain key groups. Furthermore, the new legislation affects the computing of the "transition tax" on the untaxed foreign earnings of foreign subsidiaries of U.S. companies. S corporations are also subject to the extended three year holding period for applicable partnership interests. With the new tax law changes, will come different withholding demands. The interest on home equity loans will still be deductible under the new tax law. Other items will be affected, such as the procedures for changing the accounting period of foreign corporations owned by U.S. shareholders that are subject to the transition tax under the new Tax Cuts and Jobs Act. Certain 2018 Pension Plan limitations will not be affected by the new tax law of 2017. The new law will not affect tax year 2018 dollar limitations for retirement plans. Alaska Native Corporations and Alaska Native Settlement Trusts may be able to take advantage of certain benefits that are in place in the new tax law legislation. Certain tax advantages may exist is paying items early before enacting of certain items in the new tax code take effect. One of these items is prepaid real property taxes. Real property taxes may be deductible in 2017 if assessed and paid in 2017. |

||||

| New individual and capital gains tax rates | ||||

|

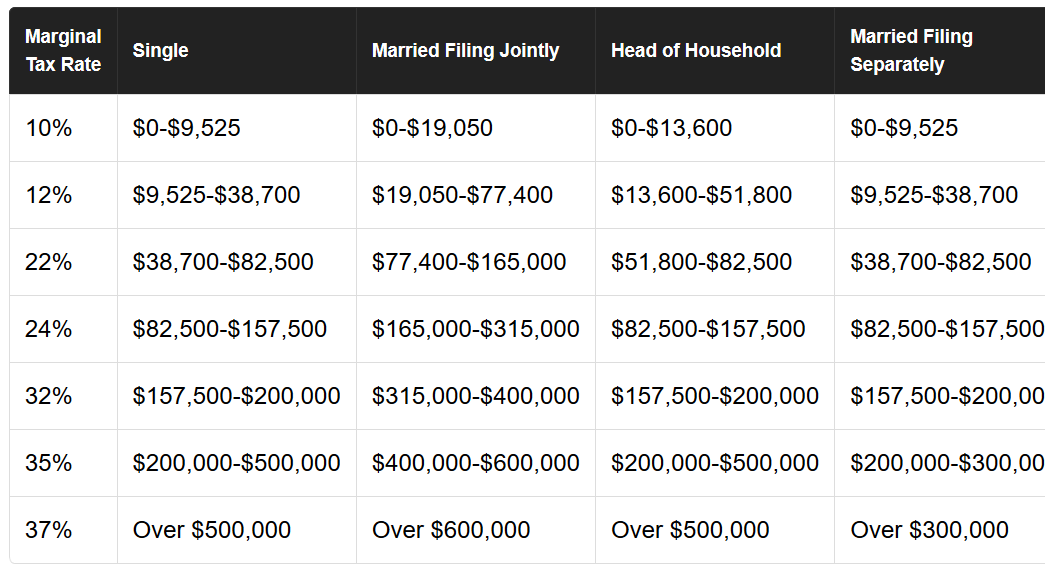

The new administration

campaign tax plan was that the number of tax brackets would reduce from

seven to three. Similarly, the House of Representatives’ original tax reform

bill contained four brackets. Ultimately, common sense interceded and we are

still at the seven-bracket structure. There is just no way, we will ever

have a postcard tax return with all these many tax brackets! The tax rates are

lower with about 2 % less than with the previous tax brackets but starting

at 10%.

The marriage penalty is almost gone. What is the marriage penalty? This penalty does not really exist as a specified penalty anywhere but it is widely talked about. Why? The marriage penalty is a concept that takes place with the change is the tax bill after a couple marries. The “marriage penalty” or the higher tax bill is due to the combined income of the couple and as a result of the combined income, the couple is changed to a new tax bracket and thus new tax rate which will usually result in paying more taxes than if the couple remained single. In a few instances the opposite can be true. Instead of a marriage penalty, the couple could incur a bonus which means that the couple fairs better by filing their tax returns as married filing jointly than when they file their tax returns as single. Thus, the couple will have a gain resulting in a bonus instead of a penalty. Again, these are widely spoken about, but there is not per say a “marriage penalty” or “marriage bonus” and these are merely the result of calculations after applying the different tax brackets at the married rates and at the single rates. Other items also affect couples that would cause a “marriage penalty” such as the ability of the individual to file as head of household when the individual is single and thus would not qualify for this HOH filing status once the individual gets married. Additionally, the individual will no longer qualify for the Earned Income Credit because of the combined income as a married individual. Remember this, the marriage penalty is not an actual penalty. It is something that happens as a result of the different tax bracket (7 tax brackets). The only thing a taxpayer can do to completely eliminate this penalty or the possibility of the marriage penalty is plan your taxes before marriage. It is a well-known fact that when couples plan to marry, the last thing on their mind is the marriage penalty. If you earn more, your income tax bracket will be higher and that only makes sense. An individual who is not married is single for tax purposes. A couple who is married is considered one individual for tax purposes and thus their income is taken together as one individual. When the couple gets married, the income will usually increase tremendously unless one of the individuals in the marriage is not working. If the income increases, then the tax bracket and the tax rate also increases. The higher tax as a result of getting married is the marriage penalty. The marriage penalty would be the higher tax and the loss of credits and deductions as a result of the marriage. What is a capital asset? Almost everything you own or use for person or investment purposes is a capital asset such as your car, household furnishings and stocks. Stocks or bonds would be items that are considered capital assets which you hold for investments. When you sell these items, the difference is a capital loss or a capital gain. Then, after that, you must determine if your assets are a short-term or a long-term item and then you will apply the tax rate. The capital gains tax rates if you have a gain, of course. If you have a loss, you usually you can deduct up to $3,000 of it. Please note that this amount is $1,500 if you are married filing separately. You have this limit and once you reach the maximum you can deduct for the year, you usually can either carry the excess forward to other years. Anyways, if you held the item for less than a year, this property is considered short-term and thus you would have a short-term capital gain and you held your asset for more than a year, then you asset is considered long-term. The tax rate on most of these capital gains is usually no more than 15% for most taxpayers. It can even be 0% if you're in the 10% or 15% ordinary income tax brackets. This is your tax bracket for your other income such as your W-2 wages. However, if you exceed certain thresholds, then your capital gains may be taxed at 20%. These thresholds are the thresholds for ordinary income tax bracket that is 39.6%. For example, if you are single and your ordinary income is $418,400 then your tax rate could be 39.6% and thus your net capital gain would be taxed at 20%. Likewise if you are married filing jointly or qualifying widow (er) that threshold is $470,700 and $444,550 for head of household. For married filing separately, this amount is almost half at $235,350. Other than being at a tax bracket of 39.6% and being taxed at the 20% capital gain rate, there are other situations. Your capital gains may be taxed at rates greater than 15% if 1. The taxable part of the capital gain from selling section 1202 qualified small business stock is taxed at a maximum 28% rate. 2. Net capital gains from selling collectible are taxed as a maximum 28% rate. 3. The portion of any unrecaptured section 1250 gain from selling section 1250 real property is taxed at a maximum 25% rate. The items discussed above usually apply only to long-term capital gains, but short term capital gains are taxed differently. Notice that net short-term capital gains are taxed as ordinary income. These gains are from property you hold for less than a year. Income is due as you earn it, so if you know you are going to have to pay capital gains tax, then you should plan accordingly and even make estimated payments. The new tax provisions in the above mentioned is that the tax rate on most net capital gain is no longer higher than 15% for most taxpayers. That is, unless you go over the thresholds mentioned or you are selling section 1202 qualified small business stock. If you are selling section 1202 qualified small business stock then it is taxed at a maximum 28% rate. Also, if you are selling collectibles your maximum rate is 28%. The portion of any unrecaptured section 1250 gain from selling this section 1250 real property is taxed at a maximum of 25% rate. Other than this, the capital gain is not higher than 15%. |

||||

| Increase in the Standard deduction and change in filing requirements for each filing status | ||||

| The new Tax Cuts and Jobs Act will increase the standard deduction amount to $12,000 for individuals, to $18,000 for head of household and to $24,000 for married couples filing jointly and surviving spouses. If you are age 65 or over, blind or disabled, you can add on $1,300 to your standard deduction if you are single, or an extra $1,600 if you are married. For individual taxpayers, you will be required to file a tax return if your gross income for the taxable year is more than the standard deduction. If you are married, you would add your spouse’s income to the picture and if the income added together is more than the standard deduction for married filing jointly, then you must file a tax return. | ||||

| Temporary reduction of personal exemption to zero | ||||

| The personal exemption which is normally adjusted for inflation every year has been changed by the TCJA to $0. Inflation works by taking a percentage of the inflation increase, but no matter how you put, anything percent of $0 will always be $0. This is to remain from January 1, 2018 through December 31, 2026. | ||||

| Adjustments to Income | ||||

|

There is an advantage in being able to claim

deductions directly from gross income - the above-the-line deductions, in

arriving at adjusted gross income. This is because these adjustments are allowed

even if you claim the standard deduction rather than the itemized deductions on

Schedule A of Form 1040. Another advantage of these over-the-line deductions is

that they also reduce state income tax for taxpayers residing in state that

compute tax based on federal adjusted gross income.

What are these adjustments to income that help you arrive at AGI? A few examples of over the line deduction that help you arrive at AGI are

These are only a few of the possible deductions that help you arrive at AGI. Adjustments to income are expenses that are applied before any taxes. These reduce your total income. These are the items you enter on your Form 1040 before you apply your standard deduction, itemized or your exemptions. After you calculate adjustments to income you are left with your adjusted gross income. Adjustments to income are individual retirement arrangement (IRAs), alimony, bad debt deduction, moving expenses, student loan interest deduction, tuition and fees deduction, and the educator expense deduction. |

||||

| Alimony | ||||

|

For almost forever, the rules have been that

alimony is deductible by the payer spouse, and the recipient spouse must include

it in income. Now with the new tax legislation, alimony is treated differently.

No longer will there be an incentive for a payer of alimony to pay alimony. Why?

This is for the simple reason that the payer will not be able to deduct it. That's why.

Before this, the payer would deduct it and the payee would have to report it in

income. Now neither can the payer deduct it, nor is the payee required to report

alimony in income because the new Tax Cuts and Jobs Act (TCJA) has changed the

alimony rules. However, there it a catch, this new law only applies for alimony

payments required by post-2018 divorce agreements. If the alimony payments are

made under a pre-2019 divorce agreement, then we continue to deduct alimony as

usual. This new tax law treatment of alimony starts for alimony divorce or

separation instruments which are executed after December 31, 2018 and thus no

more deduction for payments or including the payments in income for alimony

instruments that are executed after this date.

There are two things. The new tax law treatment of alimony payments will apply to payments that are required under divorce or separation instruments that are (1) executed after December 31, 2018 or (2) have been modified after that date and if the modification specifically states that the new tax law now applies. |

||||

| Moving expenses | ||||

|

The rules for moving expenses have changed with

the new Tax Cuts and Jobs Act (TCJA). You still need to know how the old rules

work though because based on these rules any reimbursements you get from your

employer will be taxable or nontaxable. Other than that, you will not be able to

deduct moving expenses any longer, unless you are in the military.

The requirements to deducting moving expenses are that your move closely relates to the start of work, you meet the distance test, and that you also meet the time test. If you are a member of the Armed Forces and your move was due to military order and a permanent changer of station, you don't have to satisfy the distance test. If you are in the military and have to move due to military order, you can still take a moving expense deduction on your tax return. The moving expense deduction suspension is for December 31, 2017 through December 31, 2025. Starting January 1, 2018 and beyond, you will no longer be able to deduct moving expenses on your tax return. Yes, this is another attempt at making your tax return as simple as sending in a postcard. The Tax Cuts and Jobs Act was passed in December 2017 and has eliminated the moving expense deduction. This deduction elimination is not permanent and may revert after 2025 and may depend on who is in charge at that time. It may come back at that time and at that time it will up to Congress or the individual in charge to eliminate it permanently. This means that if you moved before 2018 you may be able to claim the moving expense deduction and if you move in 2026, you may be able to claim a moving expense deduction. By the way, many of the tax law changes such as the suspension of the moving expense deduction are temporary and only for the periods of 2018 through 2025. At that time, we will know what will come back and what will stay eliminated. |

||||

| Roth IRA recharacterization rules | ||||

|

The new Tax Cuts and Jobs Act (TCJA) has removed

your ability to recharacterize your Roth IRA conversions. This could have a

major impact on financial planning for many taxpayers.

How do recharacterization work and why it is useful? A recharacterization allows you to treat a regular contribution made to a Roth IRA or to a traditional IRA as having been made to the other type of IRA. You are only allowed to make a contribution to an IRA to a certain limits and these limits are up $5,500 for 2018 or $6,500 if you are 50 or older. Different rules apply if you contribute to a traditional IRA and if you contribute to a Roth IRA or the tax treatments are different for each kind of IRA. You recharacterize by telling your trustee of the financial institution holding your IRA to transfer the amount of the contribution plus earnings to a different type of IRA which is either a Roth IRA or a traditional IRA. This is done either in a trustee-to-trustee transfer or to a different type of IRA with the same trustee. This works by making the transfer by the due date for filing your tax return (including extensions) and you treat the contribution as made to the second IRA for that year as if you made it to the second IRA for that year as if you never made it to the first IRA. Starting January 1, 2018 for tax year 2018, you will not be allowed to do this any longer as dictated with the new Tax Cuts and Jobs Act legislation. Hence, a conversion from a traditional IRA, SEP or SIMPLE to a Roth IRA can no longer be characterized. In addition, the Tax Cuts and Jobs Act also prohibits recharacterizing amounts rolled over to a Roth IRA from other retirement plans such as 401(k) or 403(b) plans. However, you have until October 15, 2018 to recharacterize a Roth IRA conversion made in 2017 and this can recharacterized as a contribution to a traditional IRA. As already discussed a Roth IRA conversion made on or after January 1, 2018 cannot be recharacterized. One thing to note is that you can still recharacterize by rolling out excess contributions to a Roth IRA. Do this if you contribute early in the year to a Roth IRA, but then earn to much over the phase-out limits, thereby disqualifying you from being able to contribute to a Roth IRA for the year. You can undo this contribution without being subject to an excess contribution penalty tax by recharacterizing the contribution to an IRA. You can still do this regardless of the new tax law changes (Hopkins 2018). It is important to note that the reason people charaterizing from one IRA to another is the fact that these are two different products that are treated differently in the tax code. With a traditional IRA for example, you get a tax deduction up front and taxes are delayed until you withdraw your money when you retire and the idea is that at that time your tax rate will be a lot lower. With Roth IRA, the IRA is funded with post-tax money and with a Roth IRA your tax rate when you retire will be zero. Therefore, recharacterizing an IRA is changing how taxes will apply to the IRA. But now, the new Tax Cuts and Jobs Act (TCJA) has removed this ability to recharacterize and this could have a major impact on financial planning for many. |

||||

| Schedule C Provisions | ||||

| We use Schedule C of Form 1040 to report our income or loss from a business or a profession as a sole proprietorship. In some rare circumstances, such as in a husband and wife operation, we use Schedule C to report income from a partnership. Your business or the kind of work that in considered Schedule C income is income that has a primary purpose of engaging in making money or in making a profit. Rarely does anyone go into business to not make money. You are usually involved in the business with continuity and regularity because you are hoping to make money from your efforts. Many individuals start out their business because they love what they do and thus their business is their passion or hobby and they end up making a lot of money from it. Well, as long as you meet the IRS rules for considering your hobby a business, then you have a business. These rules as mentioned above are that you are in the business with the primary purpose of making a profit and that you are involved in the activity with continuity and regularity. | ||||

| Elimination of entertainment expenses | ||||

|

Could it be that entertainment expense deduction

is one of the most abused business deductions and that is why it is being

eliminated? Maybe. The Tax Cuts and Jobs Act, has eliminated the entertainment

expense deduction. This new rule starts for any business activities after

January 1, 2018. The new law has done away with business entertainment expenses

for everyone - from small business owners to C corporations. No one is exempt

from this and if you are Sole-proprietor, S-Corporation, LLC, independent

contractor and business entrepreneur, this new law affects. However, don't get

us wrong. No one is telling you that you cannot entertain your customers, in

fact you must. Entertaining your customers is an integral part of doing business

regardless if you are going to get a deduction for it or not. Do yourself a

favor and don't go around telling your customers that you cannot entertain them

anymore and worst don't tell them that the new tax law does allow you to do so.

You should still entertain, but this time you, the business owner, will pick up

the tab. Regardless if it is deductible or not, entertainment expenses will

continue in business and maybe it is a shame that a business owner will not be

able to deduct these. Just because it will no longer be deductible after January

1, 2018, does not mean this activity will stop. Some will probably sacrifice

business in the name of there being no deduction for their entertainment

expenses, but many will be wise and still continue to entertain, because

entertaining their customer will continue to be a necessary business expense. At

lease in our American culture it it.

Yes, indeed, entertainment expenses are very necessary for your business to succeed. Good news, though. Remember that part of the entertainment expense that is for meals? Well, you can generally take 50% of your business-related meal expenses are allowed as a deduction. You can still entertain your customers, but you pick up the tab for the entertainment part and the IRS will pick up the tab for 50% of the meal part. To be able to deduct 50% of your meals as a business deduction though, the meal expense must be ordinary and necessary in carrying on your trade or business and this expense must still meet the directly related test or the associated test. Remember though, that these limitations only apply to your relationships with customers and not with your employees. Don't get all confused and start setting your own limits that are not included in the new Tax Cuts and Jobs Act. The expenses that are still deductible, and we mention this only so that you get this ingrained in your head, are expenses for your employees that are for 1. Entertainment, amusement and recreation expenses which you treat as compensation to your employees and of course you must include these in their wages. 2. Entertainment expenses for recreation, social, or similar activities and facilities for employees. Please note that you cannot call entertainment expenses those expenses that you incur for entertainment goods, services, and facilities which you have for sell to customers. Come on, these are called cost of goods sold. Also, again, remember that with the entertainment expense elimination as with the other elimination of deductions, that they are only temporary. The elimination is from 2018 through 2025. At that time, in 2025, we will see, how all this works out. Who knows, someone with enough sense will re-establish these provisions that have for such a long time become a part of who we are. In America we can deduct business expenses for entertaining our clients, we can golf and transact business at the same time, we can... Don't worry our America will come back to us, after all this chaos is over, we will be great again! |

||||

| New Section 179 expense limits | ||||

|

The new Tax Cuts and Jobs Act, has made

adjustments to the Section 179 depreciation limits. The Section 179 deduction

allowance was re-instated on December 18, 2015 as part of the PATH Act -

Protecting Americans from Tax Hikes Act of 2015. This act allowed the Section

179 expense to be expanded to $500,000 annually and it included a maximum bonus

depreciation of 50 percent for property put into service until December 31,

2017.

Section 179 allows taxpayers to immediately expense the cost of qualifying property rather than taking depreciation deductions in yearly increments. The maximum amount that a taxpayer can deduct has been increased with the new Tax Reform. The maximum amount a taxpayer can deduct now in Section 179 deduction for property placed in service after December 31, 2017 has been increased from $520,000 to $1,000,000. Along with this increase there is also a phase-out threshold from $2,070,000 to $2,500,000 for property placed in service after 2017. Once the amount for the total Section 179 property placed in service during the year exceeds the threshold amount, then that is when the phase out occurs and at that point the deduction will be reduced dollar-for-dollar by the excess amount. As with other tax items, the deduction and the phase-out limit amounts will be increased for inflation starting in 2019 and in later years. Under the new tax law, the qualifying property for Section 179 expensing now also includes certain depreciable tangible property used in connection with lodging and improvements to non-residential real property such as roofs, heating, ventilation, air conditioning, and fire and alarm protection systems. For many businesses and corporations, this is an excellent tax savings brought about with the new Tax Cuts and Jobs Act. |

||||

| 100% expending (Bonus Depreciation) | ||||

|

The PATH Act law states that starting January 1,

2018, bonus depreciation will begin scaling back with the ability to deduct 40

percent bonus in 2018, then 30 percent bonus in 2019. After 2019, the bonus

depreciation will be reversed to zero percent.

However, on December 22, 2017, the new tax bill went into effect increasing the deduction for bonus depreciation to 100 percent. This new tax bill will take effect immediately allow businesses to deduct 100% of eligible property placed in service after September 27, 2017, and before January 1, 2023. Some eligible property with longer production periods, the 100 percent bonus depreciation is extended through December 31, 2023. Qualifying property is property that has a depreciable recovery period of 20 years or less. Now, eligible property is expanded to include used property, certain qualified film, television, and live theatrical production equipment. The new tax law excludes property from certain utility property and vehicle dealer property. It is noteworthy that the rate of bonus depreciation will not always be 100% and it will decrease over the next four years: 80% for property placed in service in 2023 60% for property placed in service in 2024 40% for property placed in service in 2025 20% for property placed in service in 2026 0% for property placed in service after 2026 Bonus depreciation is retroactive beginning with assets purchased after September 27, 2017. |

||||

| Luxury auto limits | ||||

|

The new Tax Cuts and Job Act has also revised the

depreciation limits on luxury autos. A new luxury auto placed in service in 2018

can receive up to $18,000 in first year depreciation. The limit for luxury autos

placed in service after December 31, 2017 and in tax years that end after

December 31, 2017, are 1. $10,000 for the first year a vehicle is placed in service 2. $16,000 for the second year, 3. $9,600 for the third year, 4. $5,760 for each succeeding year until the basis in the vehicle has been recovered. The amount in 1 through 4 above will change slight to adjust for inflation. |

||||

| Listed property updates | ||||

|

Other items taken into consideration by the new

Tax Cuts and Jobs Act reform, besides luxury autos are real property and farming

property. The alternative depreciation system (ADS) recovery period for

residential rental property was shortened to 30 years for property placed in

service after December 31, 2017. There were no changes made to the ADS recovery

period for nonresidential rental property, however, and it remains at 40 years.

Farming equipment and machinery placed in service after December 31, 2017 and tax years that end after December 31, 2017, have a 5-year recovery period. Grain bins, cotton gins, fences and other land improvements are excluded from the 5-year useful life. With the new Act, there is no longer a requirement that property use in a farming business be depreciated using the 150% declining balance method. Farming property placed in service after December 31, 2017 and in a tax year ending after December 31, 2017, is depreciated using the 200% declining balance method. The 200% declining method excludes buildings, trees, vines bearing fruits or nuts, and property for which the taxpayer has elected to use either. Certain assets that can be used for business and for personal use are considered listed property and are subject to limited depreciation deductions. For example, there are limits in place for depreciating passenger vehicles and again because it is considered a personal use item. Under the new tax law, there is an increase in the annual depreciation limits on passenger autos and leading to annual limits (Section 280F limitation) of

After this the taxpayer is entitled to deduct $5,760 each year until the auto is fully depreciated. Each year a passenger auto is depreciated, the deduction is limited to the lesser of

|

||||

| Itemized Deductions Schedule A | ||||

| There have been several changes made to the tax code as a result of the new Tax Cuts and Job Act. The medical expense deduction has reverted to the 7 1/2%. State and local tax deduction has been eliminated. There have been changes to the deduction of home mortgage interest, especially for home equity loans. There will no longer be a full deduction for charitable contributions such a 60% limit on cash contributions, and not more deductions for athletic tickets. There also has been repealed with the exception to the contemporaneous written acknowledgment. Furthermore, the casualty and theft loss deduction has been limited to only federally declared disaster areas. | ||||

| Medical expenses | ||||

|

For the next two years, all taxpayers can deduct

as itemized deductions their health care expenses which exceed 7.5 percent of

their income. The new Tax Cut and Job Act did not change or restrict the ability

of taxpayers to be able to deduct medical expenses on their tax return.

Previously you could deduct only medical expenses which exceeded 10% of your

income unless you were 65 or over by the end of the year, then you can deduct

your medical expenses that exceeded 7.5 percent of your income. Now with the new

tax reform, the lower 7.5 percent has been restored for two years.

The medical expense deduction is one of the few deductions that will be left to itemize on Schedule A. The new Tax Cuts and Job Act will double the standard deduction to $12,000 for individuals and $24,000 for joint filers and with less it is anticipated that there will less taxpayers who itemize deductions on their tax returns. After the 2017 and 2018 tax years in which the 7.5 percent medical deduction threshold will be in place, the threshold will revert to the 10 percent which means a lower medical deduction. The types of eligible expenses remain unchanged. They continue to include

The items you cannot deduct continue to be the same such as over-the-counter medicines, toothpaste, cosmetic surgery, gym memberships, nutritional supplements, nicotine patches or gum and teeth whitening. |

||||

| State and local tax deduction and limit | ||||

|

The new Tax Cut and Job Act has changed our SALT.

The new tax law can have a major effect on you if you live in states like

California and New York which have large state and local taxes. A few will be

affected by the change. The SALT itemized deduction or sales and property will

be limited to $10,000 in total starting in 2018. That is a huge difference

compared to the way it has always been and since the amount of your deduction

for SALT has previously had no limit. You had a choice to deduct either your individual state income taxes paid or your sales taxes paid and for some people

this amount was up there especially if he or she lived in a state like

California or New York with high state taxes. For some people, it will not

matter too much because of the doubling of the standard deduction, but for some

it will. This is especially true for those people who have always itemized or who

will itemize because their itemized deductions end up being higher than the

standard deduction, even the doubled standard deduction.

Some taxpayers may be confused because maybe they think that this is only the state and local taxes withheld on their Form W-2. No, it is more than that. It is that plus the real estate property tax, property taxes such a the tax from the DMV taxes you pay for owning your car or cars, All these make up a huge chunk and the $10,000 cap may be way less than the actual amount spent. For some taxpayers, this deduction can mean it is $1,500 less but for other it could mean it is $18,000 or even $25,000 less. |

||||

| Home mortgage interest deduction changes | ||||

|

Under the new law, mortgage interest remains

deductible. People who own homes usually use the mortgage interest amount and

the property tax amount to come up with a reason why they would itemize because

these two amounts alone make up a large amount of their entire itemize

deductions.

There are two items you must consider in your ability to deduct home mortgage interest on your tax return. First, you will only be able to deduct the interest on the first $750,000 of your home mortgage debt. This may not matter in Bakersfield, California, for example, because homes there are way below this amount. However, in San Francisco, the median home price is $1.5 million. Second, the interest on home equity loans will no longer be deductible. Well, this only affects the loans taken out and used for purposes other than to improve the current home. Therefore, no more taking out a home equity loan to pay off your credit card and auto debt, it will no longer be deductible. Another important thing about home mortgage interest is that this applies for loans acquired after December 15, 2017, you remain unaffected by the new tax reform. You will be able to deduct your interest as you have been doing, all of it. With home equity loans, though, this is a different story as the new tax law affects even loans that were acquired before December 15. 2017. You will not be able to deduct home equity loan interest regardless of when you acquired the home equity loan. |

||||

| Charitable contribution changes | ||||

|

The new Tax Cuts and Job Act law has made the

deduction for charitable contributions better for us. It has done this by

raising the limit that can be contributed per year. The limit before was 50

percent and now it is up by 10 percent to 60 percent. Not bad, right? However,

remember these are temporary. They are little tokens to ease out of these tax

provisions.

Okay, back to charitable contribution changes. This raise is the charitable contribution deduction can be used to be able to contribute more to your favorite charitable organization and make up for the loss of deductions elsewhere. However, even though this is a positive change in the tax law code, the other changes to the code will indirectly impact contributions to charitable organizations (Miller n.d.). |

||||

| AGI limit for cash contributions | ||||

| You are allowed to contribute and deduct up to 60% of your Adjusted Gross Income (AGI) in charitable contributions. This means that if, for example, your Adjusted Gross Income is $35,000, you can contribute $21,000 of that money to your church or other favorite charitable organization and claim the entire $21,000 amount. You can donate more and faithful church goers do donate more, but the amount you can deduct will be limited to $21,000 in this example. The amount you can deduct will be limited to 60% of your Adjusted Gross Income. It used to be 50 percent before the new Tax Cuts and Job Act law passed, so we, the taxpayers, win on this one. | ||||

| No deduction for athletic tickets | ||||

|

The Tax Cuts and Job Act has repealed the rule

that allowed taxpayers to deduct 80 percent of a contribution made for the right

to purchase tickets for college and university athletic events.

Colleges and universities counted on the previous tax code that permitted the 80 percent deduction, but now they are out of luck with the new tax law reform. This means that these colleges and universities will lose millions in revenues. Many colleges and universities relied on the 80/20 rule for charitable donations to encourage athletic programs, scholarships, and other programs of the institution. If you know the rules for deducting charitable contributions when you receive a benefit in exchange, you will probably better understand the new law's position on this issue. The rules are for deducting contributions for which you get a benefit in return. If any part of your payment toward a charitable contribution is for tickets (rather than the right to buy tickets), 100% of that part is not deductible. You have to reduce the amount of your contribution by the value of any benefit you receive. However, you don't have to reduce your contribution amount if you received (1) only a small item or other benefit of token value, and (2) the qualified organization correctly determines that the value of the item or benefit you received isn't substantial and informs you that you can deduct your payment in full. The organization will be using Revenue Procedures 90-12 and 92-49 to determine this. Basically, if you receive a benefit as a result of making a contribution to a qualified organization, you can deduct only the value of your contribution that is more than the value of the benefit you receive. When you make a payment to the college or university for the right to buy tickets to an athletic event in the athletic stadium of the college or university, you are getting a benefit in return: the right to buy tickets and usually this gives you the right to buy tickets for a designated area of the stadium or some form of preference. After January 1, 2018, you longer are able to do this and get a charitable contribution deduction. However, if you pay $300 to the university for tickets for which you would normally pay $75, then you can possibly deduct the difference as a charitable contribution. As long as the organization you pay this to is a qualified organization and the event usually would have to be for charitable purposes. |

||||

| Repeal of exception to contemporaneous written acknowledgement | ||||

|

A taxpayer would not be allowed to claim a tax

deduction for any single item contribution of $250 or more unless the taxpayer

obtains a contemporaneous written acknowledgement of the contribution from the

recipient. The organization does not incur a penalty if it does provide a

written acknowledgement. However, if the organization does not provide the written

acknowledgement, the taxpayer will not be able to deduct it as an itemized

deduction on his or her tax return. This written acknowledgment requires that

the taxpayer provide on it the name of the organization, the amount of cash

contribution, and a description, without needing to disclose the value, of

non-cash contributions. Additionally, the taxpayer is required to provide a

statement from the donee that no goods or services were provided by the

organization in return for the contribution, unless there was an exchange.

Furthermore, the taxpayer must substantiate on this contemporaneous

acknowledgment a description of and a good faith estimate of the value of goods

or services, if that was the case, that the organization provided in exchange

for the contribution and you would only be able to deduct what exceeds this

value. Finally, the acknowledgment should include a statement that goods or

services consisted entirely of religious benefits, and if so the organization

would simply state that the organization provided intangible religious benefits

to the taxpayer.

Contemporaneous means that the donor receives the acknowledgment by the earlier of

The taxpayer can provide another form of substantiation such a thank you letter from the organization as long as this other form of substantiation provides the same information of the donee organization. Alternatively, the taxpayer could provide the Internal Revenue Code permitted the charitable organization to file a document with the IRS containing detailed information about the donor and his or her donation. However, with the new Tax Cuts and Job Act, this alternative process has been eliminated. Consequently, this does not seem to be a problem, since most charitable organizations usually send thank you letters to their donors. It only makes sense that they do because they want the contributions to keep coming. The donor taxpayer can use this letter as substantiation that they have made the donation. That's it with the changes to charitable contributions in the new Tax Cuts and Job Act - the alternative gift substantiation for gifts of $250 or more has been eliminated. There are other items to consider though. The fact that Congress has doubled the standard deduction means that less individuals will donate because there will be no tax incentive to do so since many people will not itemize due to the larger standard deduction. So this in itself will affect charitable organizations, indirectly. No really, indirectly because the organization will lose billions annually and this is very direct. Don't you think? Another change in the new law that will affect charitable organization is the fact that the new tax law increased the estate tax threshold and this means that fewer estates will be subject to taxation and again affecting indirectly the pockets of the charitable organization by having less bequests to charitable organizations. On a good note, the new law has increased the Adjusted Gross Income limits for cash contributions from 50 percent to 60 percent. 10 percent increase means more money from donors to the charitable organizations. |

||||

| Casualty and Theft loss deduction limited to only federally declared disaster areas. | ||||

|

One of the many deductions that you were able to claim on your tax return

was the casualties and theft losses.

To deduct a casualty or theft loss, you had to be able to prove that you

had a casualty or theft. Your records also must have been able to support the

amount you wanted to claim. For a casualty loss, your records should show the type

of casualty and when it occurred, that the loss was a direct result of

the casualty and that you were the owner of the property. To deduct a

casualty or theft loss, you must be able to prove that you had a

casualty or theft. For a theft loss, your records should show when you

discovered your property was missing, that your property was stolen and

that you were the owner of the property. Casualty and theft loss

deductions on Schedule A cover fire, storm, shipwreck, theft and other

casualty. The deduction has two limitations to qualify and they are (1)

a loss that exceeds $100, and (2) aggregate losses can be deducted only

to the extent they exceed 10 percent of adjusted gross income.

Why mention this if the deduction has been eliminated? Well, the deduction is still in effect for individuals who are victims of a federally declared disaster area and with the same terms as before the change. The exception is that the limitation is to be able to claim the deduction, you would have to be a victim of a federally disaster declared by the President under the section 401 of the Robert T. Stafford Disaster Relief and Emergency Assistance Act. Otherwise, the ability to deduct casualty and theft loss deductions has been eliminated with the new tax law. That is, unless as previously state, the loss is due to a federally declared disaster area. Many are saying that this deduction has been limited to, or severely limited. While this is sort of true, it actually has been eliminated. Just like the deduction for moving expenses that is only available to the military, the casualty and theft loss deduction is only available for victims of federally declared disaster areas. This is the exception, a casualty and theft loss deduction for a federally declared disaster area and we definitely had many of those disaster areas in the recent years. By October 2017, Americans had experienced at least 15 natural disasters for the 2017 year and then after that we had the California wild fires and mud slides. The 2017 year broke record as far as natural disasters were concerned. If the affected taxpayer has personal casualty gains, the personal casualty losses can still be offset against those gains and in this case the losses don't need to be incurred a federal declared disaster. Losses kill gains, just like when you deal with lottery winnings. The casualty gains can be offset by casualty losses and these don't have to be part of a federally declared disaster. Therefore, if you have no gain but you have losses, there is no deduction. You can have a loss deduction if it is part of federal declared disaster area regardless of gain. Hopefully, we will not have more disasters or at least not as many as we have been having. However, if we do, you need to be prepared. Are you prepared? Seriously, are your prepared if there is an earthquake or another natural disaster like the wildfires? As a tax professional, you need to be prepared to help taxpayers claims their tax deductions for a federally declared disaster area. As an individual, you need to be prepared with plenty of water and provisions. You need to be prepared with an emergency preparedness plan and everyone in your family needs to know exactly what to do in case of a disaster. |

||||

| Suspension of miscellaneous itemized deductions subject to 2% of AGI | ||||

|

Unreimbursed employee business expenses, such as

job travel, union dues, job education, et al, suspended. Tax preparation fees

which includes tax planning and consultation

fees, suspended. Miscellaneous itemized deductions, which are normally

attributed to the production of income, suspended. Other expenses such as

investment expenses, safe deposit box, and any expenses for the production of

income, suspended. This is a huge deal because items such as hobby income

expenses that were deductible before will no longer be permitted. So therefore,

you are basically reporting the entire income without any regards to the expenses.

The suspension of this deduction brings a greater grief than what it appears to be on the surface. One example of this is the deduction for hobby losses. With this elimination, the hobby losses will be eliminated 100%. Many figure that you can take hobby expenses up to the income earned, but this is not true, well, not anymore. With the new tax law, you will be able to deduct zero of your expenses that you had to acquire hobby income. You will see that there are many other items which are affected. Another one of these items that will be greatly affected by this change that seems to be harmless is the office in the home deduction which is no longer available to employees of a company who work from home. It is quite convenient to work from home. The office in the home deduction for employees which was a deduction that you can take about the 2% of AGI is no longer an option. This new tax law has affected items as the 2% of AGI deduction and has caused chaos for many taxpayers on many different platforms. |

||||

| Suspension of overall limitation on itemized deductions | ||||

|

The Pease Limitation - the overall limitation on

itemized deductions is suspended. If you look at Schedule A of Form 1040 for

2017, on line 29 it asks "Is Form 1040, line 38, over $156,900? Well, this is

the amount for a married filing separate taxpayer. It your amount is over this

amount, the instructions ask you to look at the instructions because your

itemized deductions may be limited. Once you go to the instructions, you realize

that if you are married or anything else other than single, this amount is

different. You learn that this amount is a threshold amount and that it is

different and dependent on your filing status. For a single taxpayer this amount

is $261,500, for married filing joint and surviving spouse taxpayers this amount

is $313,800 and for head of household this amount is $287,650. You also

eventually realize that the overall limitation does not reduce itemized

deductions by more than 80 percent of the total.

Now with the new law, effective January 1, 2018 and before January 1, 2026, this limitation is suspended. This means that you will not be seeing this section on Schedule A for tax years 2018 through 2025. |

||||

| Credits | ||||

| The TCJA retains the historic rehabilitation tax credit of 20% but provides for the credit to be taken over 5 years rather than when the project is placed in service, which is current law. The TCJA eliminates the 10% credit. The New Markets Tax Credits (NMTC) is retained by the TCJA current law. The new TCJA tax law retains the Renewable Energy Production Tax Credit (PTC). The new TCJA tax law retains the Renewable Energy Investment Tax Credit (ITC). These and many other credits have been retained by the new TCJA tax law. Many credits have been enhanced, such as the Enhanced Child Tax Credit with its increase to $2,000 per child instead of the usual $1,000 per child. There are many other credits which have been increase, for a temporary period of time, but nevertheless have been increased and increased drastically. What is also drastic is that some credits have been completely eliminated. | ||||

| Enhanced Child Tax Credit | ||||

| Many exciting things are happening with your taxes - at least at first. It may be like all other things. Let's enjoy now and pay the price later. Some of the changes are really, really good, such as is the case with the new way of adjustments to account for inflation. The IRS will now adjust items for inflation using the Chained Consumer Price Index for all Urban Consumers (C-CPI-U) for a better measure of the inflation. | ||||

| Increase in amount to $2,000 | ||||

|

One of these is the increase of the Child Tax

Credit signed into law by President Trump. It is quite simple really. The new

amount goes from $1,000 per child to $2,000 per child. Everything else very much

remains the same as to the qualification rules and the children that qualify you

for this credit. We will see this take affect for tax year 2018 when we file our

tax returns by April 2019. Well, there is one thing that is different besides

the amount of $2,000. The new law allows for a $300 credit for other dependents

who are over the age of 17 such as your dependent parents. This $300 credit will

be a benefit for the next 5 years. After that, things may change as expected for

most of these new tax law changes.

You already know very much how it all works. As before, this tax credit will reduce your tax bill on a dollar-to-dollar basis by $2,000 now instead of the previous $1,000 per child. So now if your tax bill is $4,000, and you have two dependents, bingo, you will owe nothing. It is a nonrefundable credit so it goes against tax. We call this credit "tax killer". What do you call it? To top it off, there another credit that can be added on top of that for those who have other dependents who are over the age of 19 such as your parents. This one is $300 per each of these types of dependents. One more thing. Your income in order to claim any of the Child Tax Credits must be only up to $200,000 if you are single. That is a huge hike from the current limit of $75,000. Likewise the amount for married folks is up $400,000 and that too is a hike from the current limit of $110,000. Now more taxpayers, ones that could not take the credit because of the set limits will now be able to take the Child Tax Credit. A married couple together earning up to $400,000 are not too rich, right? |

||||

| phase-out and refundable/nonrefundable amounts | ||||

|

There are new phase-out amounts for the child tax

credit. In addition, there are new higher amounts with the passing of the new

Tax Cuts and Jobs Act (TCJA) tax reform law that allow for a child tax credit of

$2,000 per child for tax year 2018. Not only that, but there is an expansion of

the child tax credit to include $500 for each dependent who is not a qualifying

child under the age of 17 and this credit is even allowed for the dependent

parents of the taxpayer. Even the phase-out amounts for the child tax credit have

been increased. The child tax credit new rules will be good until December 31,

2025, so enjoy it while it lasts! A credit that reduces your tax liability is a nonrefundable credit. Taxpayers have many tax credits that are "tax killers" that will help them eliminate their tax liability. If the taxpayer has children, there are more options and more available credits to them than when there are credits which don't include children. The child tax credit was started to help families raise their children. Raising a child is not cheap and many struggle to make ends meet. A credit that allows for a refund after taxes have been paid such as the newly expanded child tax credit is a refundable credit. For tax year ending in 2017, the child tax credit was for $1,000 per qualifying child. This credit was gradually phased out for single taxpayers with adjusted gross income of above $75,000 and married filing joint filers of above $110,000. However, for 2018, these amounts have changed to $400,000 for married filings jointly and to $200,000 for all the others. With the Tax Cuts and Jobs Act (TCJA) the child tax credit will change starting for tax year 2018. First of all, the credit amount is now going to be $2,000 per qualifying child and the requirement that the child be under 18 still remains a requirement. Besides the age requirement of being under 17, the other rules are basically the same as the rules for claiming a dependent child. If the taxpayer is owed a refund, the child tax credit has a refundable portion of up to $1,400 for 2018. Before this same portion of the credit was a nonrefundable credit. That is a possible extra $1,400 that families can get in addition to other credits such as the Earned Income Credit and their tax withheld amounts. This means larger much needed refund checks for working families with children. In order to claim the credit, the family must have earned at least $2,500 for the tax year. The phase out for the child tax credit starts at $200,000 for a single taxpayer and $400,000 for joint filers. This means that the individual who earn over $200,000 if single or $400,000 if married will start seeing a decrease in the amount of the child tax credit to be claimed. Now with these higher phase-out limits will allow more taxpayers to claim the child tax credit. The child does not need to be a citizen to qualify the parent for the credit, but he or she does have to have a Social Security number issued by the Social Security Administration. The new thing that is new now is the ability to get the credit if you don't have a child under the age of 17. The new tax reform allows taxpayers to claim a $500 credit for dependents such as parents and other members of the household. There is no age limit for this new part of the child tax credit. How odd is that? Now you can get a child tax credit for a parent. Not only parents but other dependents too. You can claim the child tax credit for a child who is disabled and dependent you support who is a full-time student. There is still a possibility that all this good news will not last beyond 2025 as this new increase in the child tax credit and the qualification rules are set to expire by 2025 - by December 31, 2025 to be more exact. This legislation, the new Tax Cuts and Jobs Act (TCJA) has, at least for a temporary time, taking into account hard working family with a much needed refundable child tax credit which is going to make an incredible difference in the lives of kids all around the country. To top it off, the child credit has been expanded to include more children, not just the children under 17. Furthermore, the child tax credit has somehow morphed into a non-child dependent credit allowing a refund of $500 more for dependents who are not qualifying children under the age of 17. This new Tax Cuts and Jobs Act (TCJA) reform cannot possibly only be for the rich if you look into the generosity behind the new revamped child tax credit. There has been a lot of talk on national T.V. as to the new tax law being for the rich. Maybe it is for the rich starting January 1, 2026 but for now the new child tax credits disproves the theory that the new tax reform of 2017 is for the rich |

||||

| SSN Requirement | ||||

|

The Child Tax Credits have been claimed by

parents for any of their children who are under the age of 17. There were not

too many requirements to claim this non-refundable credit with the previous law

before this new tax reform. Very simply, you have a dependent who is under the

age of 17, you claim a credit against your income for that child of up to 1,000.

If your tax bill is $970 and have only one child who is under age 17, for

example, then with the $1,000 tax killer you take care of the $970 tax bill and

you owe the IRS nothing. The qualification requirements for this child to

qualify you for the child tax credit, was closer to no requirements. Any

qualifying child for this credit was someone who met the qualifying criteria of

six tests such as age, relationship, support, dependent test, citizenship or

residence test. So basically, you had a dependent under age 17, you had a credit

of $1,000 for that dependent. As far as the relationship test was concerned, it

was the same relationship test that you must pass in order to claim a dependent

so therefore it was as if this test to claim the child for the child tax credit

did not exist or it was a given as it had already been met when you could claim

the child as a dependent. Additionally and again the same as the dependent test,

the child must have not supported him or herself for more than half of their own

support and the child must have been a U.S. Citizen, U.S. national or U.S.

resident alien and must have lived with you for more than half of the year or in

sum qualify under all the tests to qualify as your dependent.

If in 2017, your modified adjusted gross income (AGI) is more than the following amounts then the amount of the $1,000 child tax credit is either reduced or totally eliminated.

Compare this to the 2018 phaseout amounts. For 2018, if your modified adjusted gross income (AGI) is more than the following amounts then the new amount of the $2,000 child tax credit is either reduced or totally eliminated.

Now with the new tax law your income in order to claim any of the Child Tax Credit, which is up to $2,000 per child by the way, must be only up to $200,000 if you are single. That is a huge hike from the current limit of $75,000. Likewise the amount for married folks is up $400,000 and that too is a hike from the current limit of $110,000. Now more taxpayers, ones that could not take the credit because of the set limits, will now be able to take the Child Tax Credit. A married couple together earning up to $400,000 are not too rich, right? Well at least that is what they say when they talk about how poor they are. If the child did not have a Social Security number, an ITIN number could be used to claim the child tax credit for the $2,000 amount. Now, under the new tax bill, children with ITIN number will need to provide a Social Security number in order to claim the child tax credit for that child since now the child tax credit is refundable. In order to claim the refundable part and the non-refundable part of the credit a Social Security number must be provided. The idea behind this is that most children who have an ITIN, have an ITIN because they are undocumented. This is going to impact the entire family because as you may be well aware of families that immigrate to the United States have both foreign born and US born children. Let's face it, we are a country that has allowed for this to happen and now in the process of trying to change things, we are hurting innocent people and United States citizens too! This new bill will directly affect those children born in the United States whose non-citizen siblings are no longer eligible for the credit and thus impacting the entire family. This situation is similar to the situation where the illegal parents are deported and it does not take a brain surgeon to know that we are also deporting American citizens in the process. What? Did you think that the American children stay behind in the United State in orphanages? Go back to the cave you peeped out of if you think that is the case and don't come out until you realize your illogical fallacy. Also if you have not realized it by now that only the rich immigrate legally, then there is definitely something wrong and you probably should rethink things - maybe not totally. We have yet to see a day laborer, for example, try to immigrate to the United States legally. Another thing to consider is the fact that not too many people who are well off in their country want to immigrate to the United States. There is always a catch. For example, students immigrate here because after they finish their studies they get used to our way of life, they make new friends and at the end they simply stay here and this group of well-educated individuals, the students, decide to stay in our country forever. Then, they force their parents to move here because the grandparents want to be with their grandchildren. You never thought of it like this, have you? Would someone remind us next time not to hire an individual to be boss who has married immigrants and who by the look of things is about to divorce another one - because this individuals start hating his ex-wives and then he wants to make all immigrants including children both American and immigrant suffer for his mistakes. If you don't want to offer tax credits to illegal immigrants, that is probably fine. But what is not fine is that you charge them taxes just like U.S. Citizens. We keep hearing these senseless individuals saying that they want only people who play the rules to be rewarded - then you must allow the less fortunate to be able to play by the rules. Let's face it - immigration laws do not allow people who don't have money to play by the rules. Let's do it - Let's not allow undocumented immigrants to receive any tax benefits but you cannot tax them either. Are we ever going to learn from our history? Let's go back to 1761 and recall the phrase "No taxation without representation!" Maybe someday, good sense and fairness will enter our vocabulary once again. Quit your excuses and self-serving righteousness to steal other people's money. When you tax individuals and rob them of their right to receive tax benefits available to others who pay exactly the same, you are technically stealing their money. |

||||

| New $500 nonrefundable credit for dependents other than a qualifying child or for a qualifying child without the required SSN | ||||

|

The Tax Cuts and Jobs Act (TCJA) has dramatically

changed things. The child tax credit is really now a misnomer. How we can keep

calling a credit that does not any longer only apply to children child tax

credit? The child tax credit is a credit which allowed for $2,000 credit per

qualifying child under the age of 17. The child tax credit met certain

thresholds which reduced the child tax credit $50 for every $1,000 for which

adjusted gross income (AGI) exceeded $400,000 for married filing jointly

individuals, $200,000 for married individuals filing separately, and $200,000 for

single taxpayers. Then part of the child tax credit was considered a refundable

credit when taxpayer had more than three children. The excess of the taxpayer's

social security taxes for the year over the earned income credit for the year

was refundable. However, in all cases the refund was limited to $1,000 per

qualifying child under the age of 17.

Now amongst other things, the new TCJA tax reform will double the child tax credit from $1,000 to $2,000 per qualifying child under age 17. Furthermore, get a hold of this, the new TCJA tax reform allows for a new $500 credit per any of the dependents who are not qualifying children under 17. As long as they are your dependents and pass the dependent tests, there is no age limit for this $500 credit. It seems very much that we need to change the name of this credit from child tax credit to child and dependent tax credit. This new child tax credit, however, is nonrefundable. To be able to claim the child tax credit for a qualifying child, you must have a SSN for the child. The previous law permitted taxpayers to use individual taxpayer identification numbers (ITIN) or adoption taxpayer identification numbers (ATIN). Now with the new ICJA tax reform, it specifically states that if the child does not have a Social Security Number (SSN), you will not be permitted to claim the $2,000 credit. However, you will still be allowed to claim the $500 credit for that child using an individual taxpayer identification number (ITIN) or an ATIN. Although the SSN requirements don't apply for a non-qualifying child dependent, you still must provide an ITIN or an ATIN for each dependent in order to claim the $500 child tax credit. |

||||

| Alternative Minimum Tax (AMT) - increase in exemption /phase-out amounts | ||||

|

The alternative minimum tax will continue in the

new Tax Cuts and Jobs Act (TCJA). However, now the alternative minimum tax has

been adjusted to apply to higher income taxpayers. The new tax rules start

apply for tax year 2018 which hopefully we will not be trying to do last minute

figuring out and be running around like chickens without a head.

We all should know by now how the AMT works by now. We have two separate tax systems, one is the regular tax system and the other is the AMT tax system. The alternative minimum taxes certain types of income that have been used to claim certain credits and deductions under the regular tax system and ultimately disallows some tax breaks allowed in the other tax system. The good news is you have really good tax breaks. The bad news is that you owe ATM tax and those good tax breaks we mentioned before are no longer applicable. That is the common story behind the alternative minimum tax. The purpose of the AMT is to effectively take back some of the tax breaks allowed for regular tax purposes. The AMT is an additional tax that you may owe if for regular tax purposes you claimed:

There are no specific tests to determine whether or not you are liable for the alternative minimum tax (AMT). You must first figure your regular income tax and then see whether tax benefit items must be added back to taxable income to figure alternative minimum taxable income, on which the AMT is figured. If after claiming the AMT exemption and applying the AMT rate and the tentative alternative minimum tax exceeds your regular income tax, the excess is your AMT liability, which is added to the regular tax on your return. In other words, your tax liability for the year will the greater of your regular tax or your alternative minimum tax (AMT). With the new Tax Cuts and Jobs Act (TCJA) rules, the maximum AMT rate will only be 28 percent. That is huge improvement for the taxpayer from the previous 39.6 percent maximum rate that applied under the previous old law. Previously, the 28 percent AMT rate kicks in when AMT income exceeds $187,800 for married filing joint filers and $93,900 for the rest. However, for 2018 and beyond, the 28% AMT rate starts only when AMT income exceeds $191,500 for married filing joint filers and $95,750 for the others. To make things better, you are allowed an AMT exemption and it is deducted when you are calculating the AMT income. This exemption amount is significantly increases for tax years 2018 through 2025. Once the AMT surpasses the applicable threshold, the exemption amount is phased out. However, those thresholds are also very generous and the TCJA has greatly increased them for tax years 2018 through 2025. The TCJA has increased the individual AMT exemption amounts for tax years 2018 through 2025 to $109,400 for married filing joint filers and surviving spouses, to $70,300 for single filers, and to $54,700 for married filing separate filers. Once the taxpayer's alternative taxable income is above $1 million and $500,000 for the other taxpayers, the increased exemption amounts are reduced by 25% of the amount of the taxpayer's AMT income above these amounts. Notably, the increased exemption amounts will not be reduced below zero. It is important to plan your taxes and try to avoid being hit by the AMT. However, it may be a bit difficult to try to pinpoint what will trigger the alternative minimum tax since there are so many factors involved. First, high income can cause the AMT exemption to be partially or completely phased out and this would a factor that increases your chances of owing the alternative minimum tax. The TCJA has lowered some of its regular tax rates (5 of them) while leaving the AMT rates at 26 percent and 28 percent will definitely not help you in trying to avoid the AMT. Other items that may cause you to own the AMT are large itemized deductions that include deductions for state and local taxes. This is especially true since these taxes are completely disallowed under the new AMT rules. The new tax law limits the regular tax deduction for state and local income taxes and property taxes combined to $10,000 ($5,000 if married filing separate). Another item that may cause you to trigger the AMT is having too many personal and dependent exemptions because these are completely disallowed under the AMT rules. This is specially true since for 2018 through 2025, personal and dependent exemption deductions are completely eliminated under the new TCJA tax reform. Incentive Stock options (ISOs) do not count as income under the regular tax rules but they do count as income under the alternative minimum tax rules. So if you have these (no change from the old rules), you may trigger the AMT. You can no longer include investment expenses, fees for tax advice and tax preparation and unreimbursed employee business expenses for itemized deductions under the new tax rules. However, under the old tax law or under the new these items remain as disallowed for the alternative minimum tax, therefore, this would not be a trigger for the AMT, at least this time around. Other items that would be of interest to look into for possible triggers of the AMT are interest income from privacy activity bonds, claiming the standard deduction since it is now almost doubled. The new tax law no longer allows a deduction for home equity loan interest, so therefore, this is not an item of threat or that would trigger the AMT. The alternative minimum tax (AMT) liability is figured on Form 6251 and is attached to Form 1040. If you file Form 1040A, AMT liability, if any, is figured on a worksheet and the AMT is included on the line for "Tax" on Form 1040A. After you determine your regular income tax liability, you use Form 6251 to compute AMT liability, if any. |

||||

| 20% deduction for a pass through qualified trade or business | ||||

|

The TCJA of 2017 has brought changes to the way

pass through qualified trade or business handles its deductions. A qualified

pass-through business income deduction will permit its shareholders to deduct

20% of the business income and will be claimed as a below-the-line deduction for

tax purposes. However, the new tax rules do not permit the deduction for

high-income "Specified Services" businesses which includes lawyers, accountants,

doctors, consultants, and financial advisors. High income individuals may have

their QBI deduction limited if they do not employ a substantial number of people

relative to the size of the business under the new "W-2 wages" limit.

Additionally, they may have their QBI deduction limited if they invest into a

substantial amount of property under the "wages-and-property" limit.

The new rules make it easier for a small business to claim at least a modest new QBI deduction and this deduction is available even if the small business is sole proprietorship which means that it is not actually necessary to have an actual business entity like a partnership, LLC or an S-corporation. This deduction is even greater for large scale businesses. On the other hand, a business who primarily relies on the efforts of its owners, whether they are Specified service business, or those that have a limited amount of employees or capital investments, may find taking QBI deduction a bit more complicated. Especially noticeable in this case would be individual who are over the new income threshold of $157,500 for individuals and $315,000 for married filing jointly. The new deduction for pass-through businesses was created by the Tax Cuts and Jobs Act (TCJA) and this deduction can allow you to take a deduction for up to 20% on income from your sole proprietorship, partnership and other business such as S corporations that are pass-through businesses. The amount of the deduction that you can take will vary depending on

There are two classes of businesses taken into consideration for the 20% deduction. First class of business is the business that provides certain personal services such as law firms, medical practices, consulting firms and professional athletes. In the second class are all the other businesses that are not part of the previously mentioned. After that, the business owners are divided into three groups such as